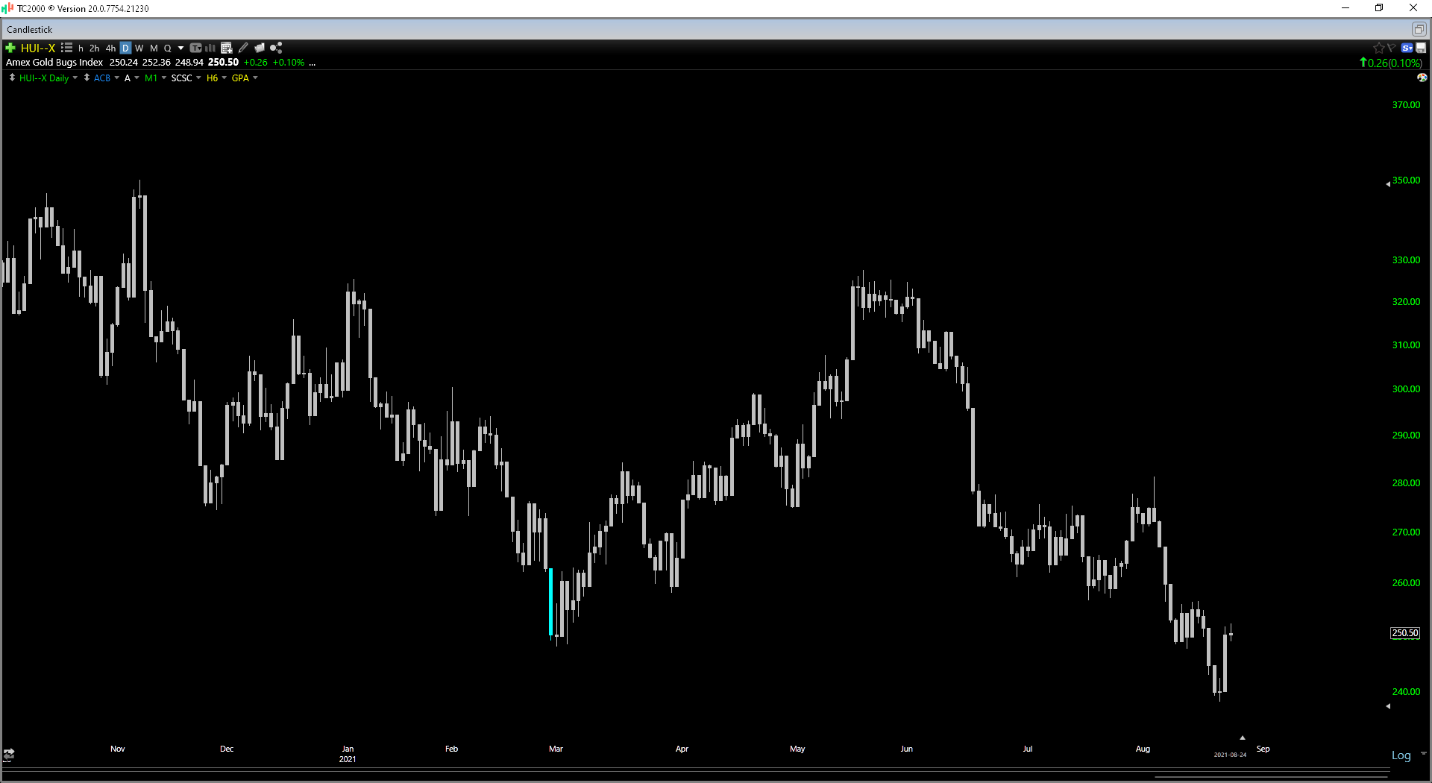

It’s been a disappointing year thus far for the Gold Miners Index (GDX), with the ETF down more than 10% year-to-date and more than 30% from its new highs 12 months ago. Given the backdrop with high inflation readings and continued money printing, the returns are even more disappointing, causing many to abandon the sector altogether in search of greener pastures. Fortunately, despondence breeds opportunity, and any time that a sector is the most hated it’s been in years, it’s time to be open-minded about a potential bottom in the market and much better returns ahead. This bodes well for the GDX over the medium-term, especially because this correction in the ETF this different. Unlike past corrections, the average GDX constituent is in much better financial shape, is paying a dividend, and is generating significant free cash flow with gold prices above $1,600/oz. In this update, we’ll look at three names that stand out as buy-the-dip candidates, with these being SSR Mining (SSRM), Newmont (NEM), and Hecla Mining (HL).

(Source: TC2000.com)

Hecla Mining, SSR Mining, and Newmont all offer differing exposure to the metals space. One is a silver producer, the second is a silver & gold producer, and the latter is the largest gold producer in the world. However, they all share one key trait, industry-leading margins with some of the best cost profiles in the sector. In Newmont’s case, the company has recently seen inflationary pressures but continues to benefit from silver/copper by-products which are pulling its costs down. In Hecla’s case, the company is one of the highest-grade silver producers globally and the only large-scale silver producer operating out of solely Tier-1 jurisdictions. Finally, SSR Mining has recently beefed up its production profile, merging with Alacer Gold to create a diversified global producer with gold production in the United States and Canada, silver production in Argentina, and gold/copper production in Turkey. Based on recent estimates, these companies are all trading at less than 18x FY2022 earnings estimates despite 40% plus margins while also returning considerable value to shareholders through dividends and buybacks. Let’s take a closer look at each company below:

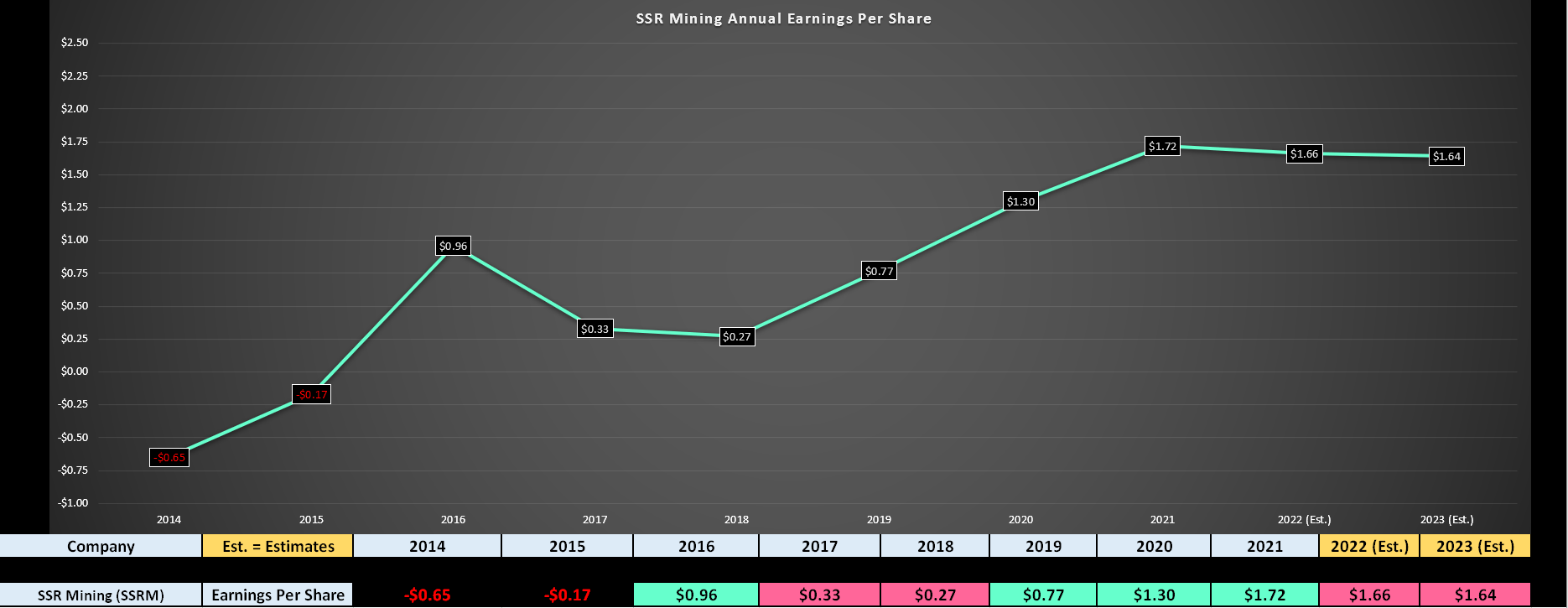

Beginning with SSRM, the company just came off another solid quarter, reporting quarterly production of ~199,700 GEOs, up 2% from Q1 2021 and more than 78% on a two-year basis. This massive increase in production can be attributed to the acquisition of the Copler Mine in Turkey, which was closed last quarter. Not only does this asset give SSRM a third gold mine and diversify its production profile, but the deal was accretive on margins, with Copler producing nearly ~250,000 GEOs per annum at all-in sustaining costs below $850/oz. Given the exploration potential on the property, there is the possibility that SSR Mining can grow production to ~300,000 GEOs per annum with the Ardich deposit, giving SSRM a path to producing ~850,000 GEOs per annum, or high single-digit growth from current levels. Concurrently, SSRM is aiming to increase its production base at Marigold, hunting down higher-grade deposits to supplement its current low-grade heap-leach operations.

(Source: YCharts.com, Author’s Chart)

Given the company’s solid operating performance in Q2, SSRM reported a near-record free cash flow figure of $100.4 million and is on track to generate up to $300MM in free cash flow in FY2021 alone. For a company with an enterprise value of just ~$3.0BB, this is a dirt-cheap valuation. Notably, SSR Mining is also committed to returning value to shareholders, buying back over 6MM shares (2.5% of float) since April, and starting to pay a dividend of US$0.05 per quarter. If we combine this aggressive buyback program and dividend with the stock trading at just 9x FY2021 earnings estimates, the stock looks very reasonably valued here. So, if the stock were to dip to support at $15.05, I would view this as a low-risk buying opportunity.

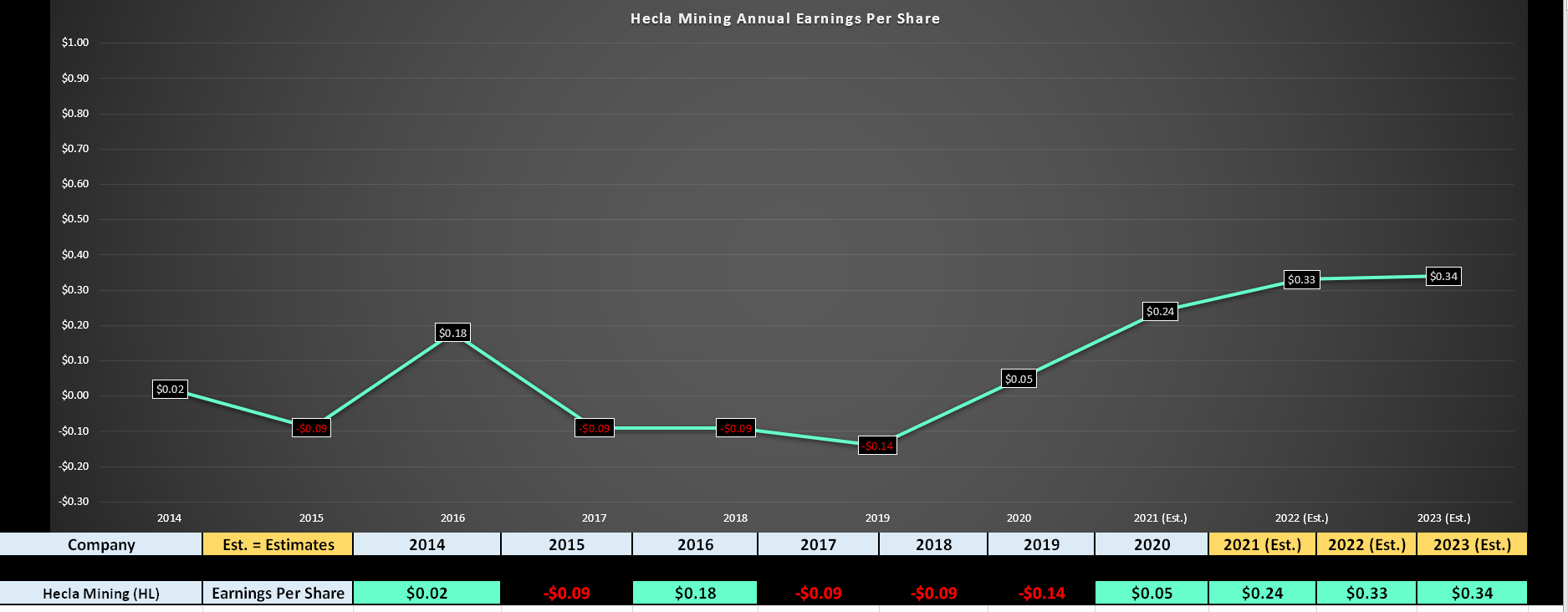

Moving over to Hecla Mining, the company had a solid quarter as well, reporting production of ~3.52 million ounces of silver and ~59,100 ounces of gold, translating to ~10.1 million silver-equivalent ounces [SEOs]. This makes HL one of the largest primary silver producers globally, and with the potential to access higher grades at its Lucky Friday Mine, production should grow even further in FY2022. While Hecla’s production was impressive given that the company was lapping strong year-over-year results, it was the costs that really shined in Q2, dropping to just $7.54/oz. This translated to a decline of 19% year-over-year and translated to all-in sustaining cost margins of 72%. These are some of the most impressive margins in the sector currently, making HL deserving of a premium valuation vs. its silver producer peers.

(Source: YCharts.com, Author’s Chart)

While margins are likely to dip in H2 due to a much weaker silver price, HL should still boast 55% plus AISC margins, and this H2 softness is beginning to get priced into the stock. This is because HL has fallen more than 40% from its 52-week highs and now trades at just 18x FY2022 earnings estimates. While this does not offer a significant margin of safety like NEM, which we’ll discuss later, the valuation is beginning to get more compelling. So, if HL were to dip below $5.00 before year-end, where it would slide to ~16x earnings, I would view this as a low-risk buying opportunity.

The final name on the list is Newmont Corporation (NEM), the largest gold producer globally and one of the few members of the S&P-50 that’s paying a 3.75%+ plus dividend yield. During Q2, NEM had a tough quarter, with production up sharply year-over-year, but down 8% on a two-year basis. This was due to continued COVID-19 headwinds in South America, home to a few of Newmont’s mines. This was offset by significantly higher gold-equivalent ounce production that more than doubled (303,000 vs. 111,000) on a two-year basis, but analysts focused on the cautionary guidance. This included the potential for costs to come in at the high end of the guidance range due to inflationary pressures, which will weigh on Newmont’s profitability a little.

Having said that, even if costs come in at $1,000/oz, NEM is still generating an AISC margin of more than $775/oz at current levels or ~44% at a $1,775/oz gold price. These margins are quite enviable compared to the average profit margin of less than 20% for S&P-500 companies and better than the sector average of 40%. Besides, Newmont expects to see costs improve in FY2023 once capex is reduced, with the potential for all-in sustaining costs to dip below $900/oz. Finally, NEM continues to invest in innovation, with an autonomous haulage fleet rolled out at its massive Boddington Mine and plans to continue to roll out autonomous drill rigs and haulage at more mines over the next few years. This should offset inflation in fuel with a shift to more renewable energy and also offset any labor inflation/costs.

(Source: YCharts.com, Author’s Chart)

During the most quarter, the company reported revenue of $3.07BB and free cash flow of $580MM and is on track to report annual EPS of more than $3.80 next year. At a share price below $57.00, this translates to a P/E ratio of just 15, which is a dirt-cheap valuation for a company with NEM’s margin profile. The bonus is that investors get a 3.75% yield to look forward to, with NEM paying a quarterly dividend of $0.55 per share. Notably, NEM could raise this dividend to $2.80 by FY2023 even if gold prices stay in the $1,650/oz to $1,900/oz range, which is the upper edge of its payout ratio. This would give investors a 4.9% yield on cost. So, for investors looking for stability and a mix of both growth and value, NEM looks like a steal here at $57.00 per share.

It’s easy to be pessimistic on the gold sector after poor returns the past 12 months, but it’s exactly at these times when it’s best to be optimistic, especially when you have investors flooding into riskier assets each day. In investing, the most consistent way to generate alpha and outsized returns is doing the opposite of the majority and buying the best companies possible with a margin of safety baked in when a sector is hated. Currently, NEM meets this criterion, and HL and SSRM would meet these criteria at a share price of $15.00 and $5.00, respectively. So, for investors looking for an area of the market to begin to nibble where they can enjoy a margin of safety and a yield, I see these three names as ones to keep near the top of one’s shopping list.

Disclosure: I am long GLD, NEM

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

NEM shares were trading at $56.68 per share on Thursday afternoon, down $0.23 (-0.40%). Year-to-date, NEM has declined -3.72%, versus a 20.39% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post 3 Miners Trading At Dirt-Cheap Valuations appeared first on StockNews.com