The end of an earnings season can be a great time to discover new stocks and assess how companies are handling the current business environment. Let’s take a look at how Yum China (NYSE:YUMC) and the rest of the traditional fast food stocks fared in Q3.

Traditional fast-food restaurants are renowned for their speed and convenience, boasting menus filled with familiar and budget-friendly items. Their reputations for on-the-go consumption make them favored destinations for individuals and families needing a quick meal. This class of restaurants, however, is fighting the perception that their meals are unhealthy and made with inferior ingredients, a battle that's especially relevant today given the consumers increasing focus on health and wellness.

The 14 traditional fast food stocks we track reported a mixed Q3. As a group, revenues were in line with analysts’ consensus estimates.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 8.1% since the latest earnings results.

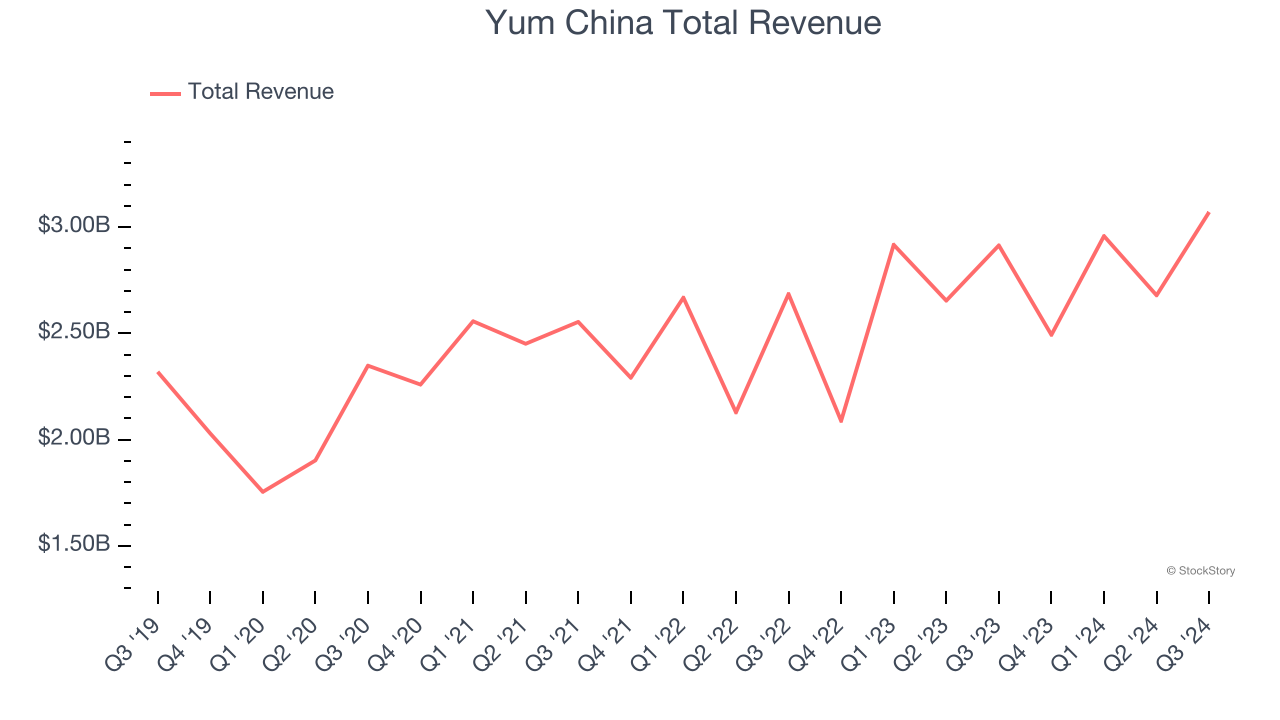

Yum China (NYSE:YUMC)

One of China’s largest restaurant companies, Yum China (NYSE:YUMC) is an independent entity spun off from Yum! Brands in 2016.

Yum China reported revenues of $3.07 billion, up 5.4% year on year. This print exceeded analysts’ expectations by 1.5%. Overall, it was a strong quarter for the company with an impressive beat of analysts’ EBITDA estimates and a decent beat of analysts’ EPS estimates.

Joey Wat, CEO of Yum China, commented, "We delivered strong results again in the third quarter. Operating profit increased by 15%, core operating profit grew 18%, and diluted EPS increased by 33%."

The stock is down 3.6% since reporting and currently trades at $43.42.

Is now the time to buy Yum China? Access our full analysis of the earnings results here, it’s free.

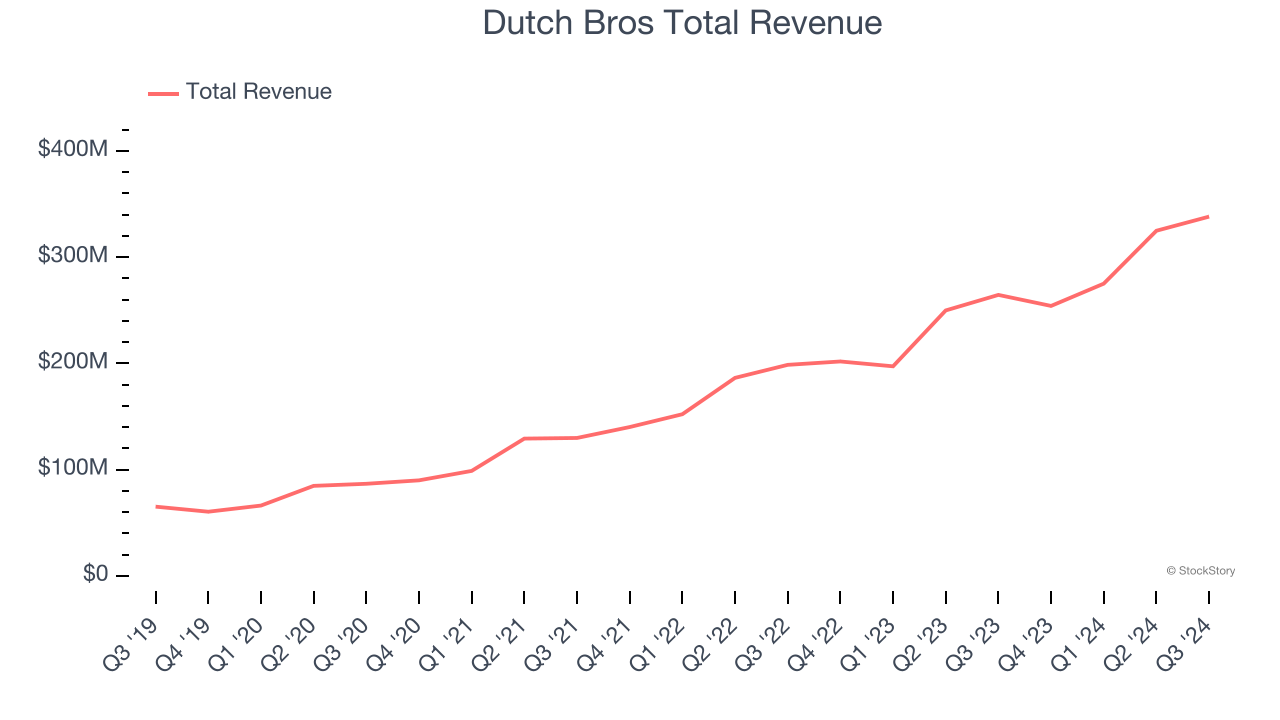

Best Q3: Dutch Bros (NYSE:BROS)

Started in 1992 by two brothers as a single pushcart, Dutch Bros (NYSE:BROS) is a dynamic coffee chain that’s captured the hearts of coffee enthusiasts across the United States.

Dutch Bros reported revenues of $338.2 million, up 27.9% year on year, outperforming analysts’ expectations by 4.1%. The business had a stunning quarter with an impressive beat of analysts’ EBITDA estimates and a solid beat of analysts’ same-store sales estimates.

Dutch Bros pulled off the biggest analyst estimates beat, fastest revenue growth, and highest full-year guidance raise among its peers. The market seems happy with the results as the stock is up 60.6% since reporting. It currently trades at $56.07.

Is now the time to buy Dutch Bros? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: Krispy Kreme (NASDAQ:DNUT)

Famous for its Original Glazed doughnuts and parent company of Insomnia Cookies, Krispy Kreme (NASDAQ:DNUT) is one of the most beloved and well-known fast-food chains in the world.

Krispy Kreme reported revenues of $379.9 million, down 6.8% year on year, in line with analysts’ expectations. It was a disappointing quarter as it posted a significant miss of analysts’ EBITDA and EPS estimates.

Krispy Kreme delivered the slowest revenue growth and weakest full-year guidance update in the group. As expected, the stock is down 27.4% since the results and currently trades at $9.02.

Read our full analysis of Krispy Kreme’s results here.

Wendy's (NASDAQ:WEN)

Founded by Dave Thomas in 1969, Wendy’s (NASDAQ:WEN) is a renowned fast-food chain known for its fresh, never-frozen beef burgers, flavorful menu options, and commitment to quality.

Wendy's reported revenues of $566.7 million, up 2.9% year on year. This print beat analysts’ expectations by 1.2%. Zooming out, it was a mixed quarter as it also logged full-year EBITDA guidance slightly topping analysts’ expectations but a slight miss of analysts’ same-store sales estimates.

The stock is down 24.8% since reporting and currently trades at $15.27.

Read our full, actionable report on Wendy's here, it’s free.

Papa John's (NASDAQ:PZZA)

Founded by the eclectic John “Papa John” Schnatter, Papa John’s (NASDAQ:PZZA) is a globally recognized pizza delivery and carryout chain known for “better ingredients” and “better pizza”.

Papa John's reported revenues of $506.8 million, down 3.1% year on year. This number surpassed analysts’ expectations by 1.6%. However, it was a mixed quarter as it logged a slight miss of analysts’ same-store sales estimates.

The stock is down 33% since reporting and currently trades at $39.

Read our full, actionable report on Papa John's here, it’s free.

Market Update

Thanks to the Fed's series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market has thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% each in November and December), and a notable surge followed Donald Trump's presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by the pace and magnitude of future rate cuts as well as potential changes in trade policy and corporate taxes once the Trump administration takes over. The path forward is marked by uncertainty.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.