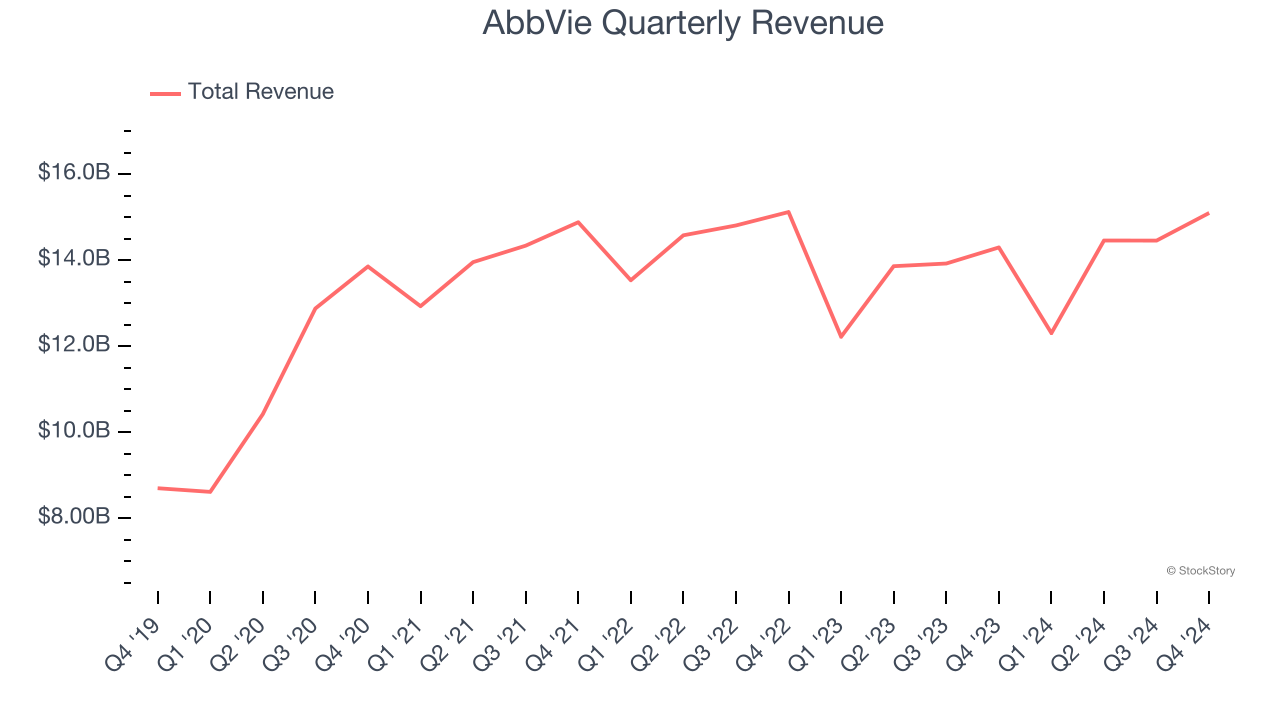

Pharmaceutical company AbbVie (NYSE:ABBV) reported Q4 CY2024 results topping the market’s revenue expectations, with sales up 5.6% year on year to $15.1 billion. Its non-GAAP profit of $2.16 per share was 4.3% below analysts’ consensus estimates.

Is now the time to buy AbbVie? Find out by accessing our full research report, it’s free.

AbbVie (ABBV) Q4 CY2024 Highlights:

- Revenue: $15.1 billion vs analyst estimates of $14.82 billion (5.6% year-on-year growth, 1.9% beat)

- Adjusted EPS: $2.16 vs analyst expectations of $2.26 (4.3% miss)

- Adjusted EPS guidance for the upcoming financial year 2025 is $12.22 at the midpoint, beating analyst estimates by 0.8%

- Operating Margin: -9.9%, down from 22.3% in the same quarter last year (negative margin caused by non-recurring impairment and amortization charges)

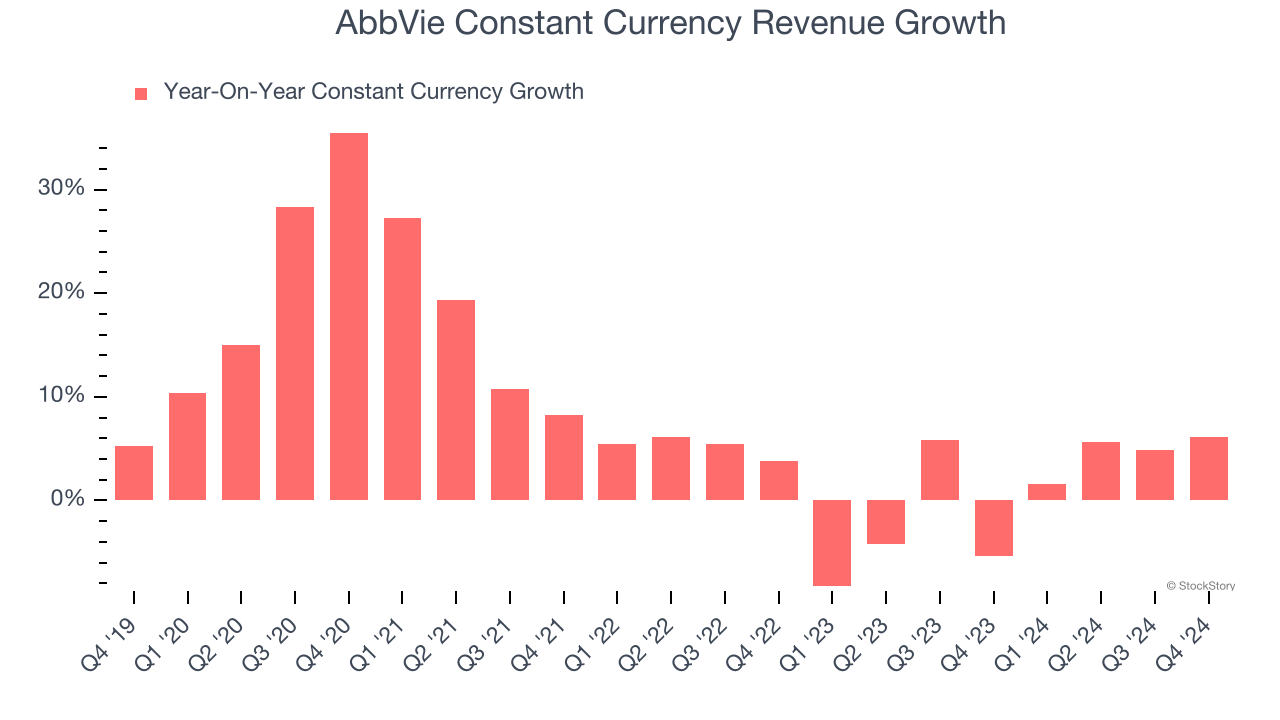

- Constant Currency Revenue rose 6.1% year on year (-5.4% in the same quarter last year)

- Market Capitalization: $310.4 billion

"2024 was a year of significant progress for AbbVie. Our growth platform delivered outstanding results, we advanced our pipeline with key regulatory approvals and promising data, and we strengthened our business through strategic transactions," said Robert A. Michael, CEO of AbbVie.

Company Overview

Founded in 2013 as a spin-off from Abbott Laboratories (NYSE:ABT), AbbVie (NYSE:ABBV) is a biopharmaceutical company that develops and sells prescription medicines focused on areas like immunology (arthritis, for example), oncology (cancers), and neuroscience (depression, for example).

Therapeutics

Over the next few years, therapeutic companies, which develop a wide variety of treatments for diseases and disorders, face strong tailwinds from advancements in precision medicine (including the use of AI to improve hit rates) and growing demand for treatments targeting rare diseases. However, headwinds such as rising scrutiny over drug pricing, regulatory unknowns, and competition from larger, more resourced pharmaceutical companies could weigh on growth.

Sales Growth

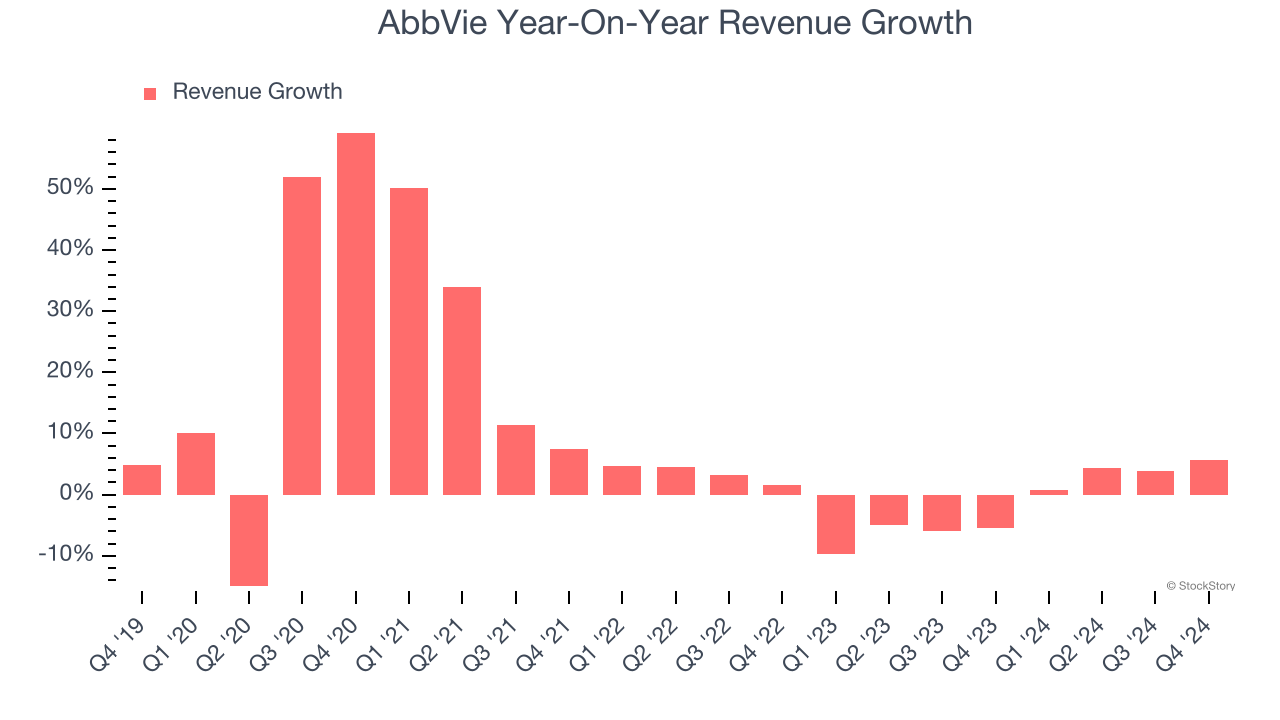

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, AbbVie grew its sales at a decent 8.6% compounded annual growth rate. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. AbbVie’s recent history marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 1.5% over the last two years.

AbbVie also reports sales performance excluding currency movements, which are outside the company’s control and not indicative of demand. Over the last two years, its constant currency sales were flat. Because this number is better than its normal revenue growth, we can see that foreign exchange rates have been a headwind for AbbVie.

This quarter, AbbVie reported year-on-year revenue growth of 5.6%, and its $15.1 billion of revenue exceeded Wall Street’s estimates by 1.9%.

Looking ahead, sell-side analysts expect revenue to grow 5% over the next 12 months, an improvement versus the last two years. This projection is above average for the sector and indicates its newer products and services will catalyze better top-line performance.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

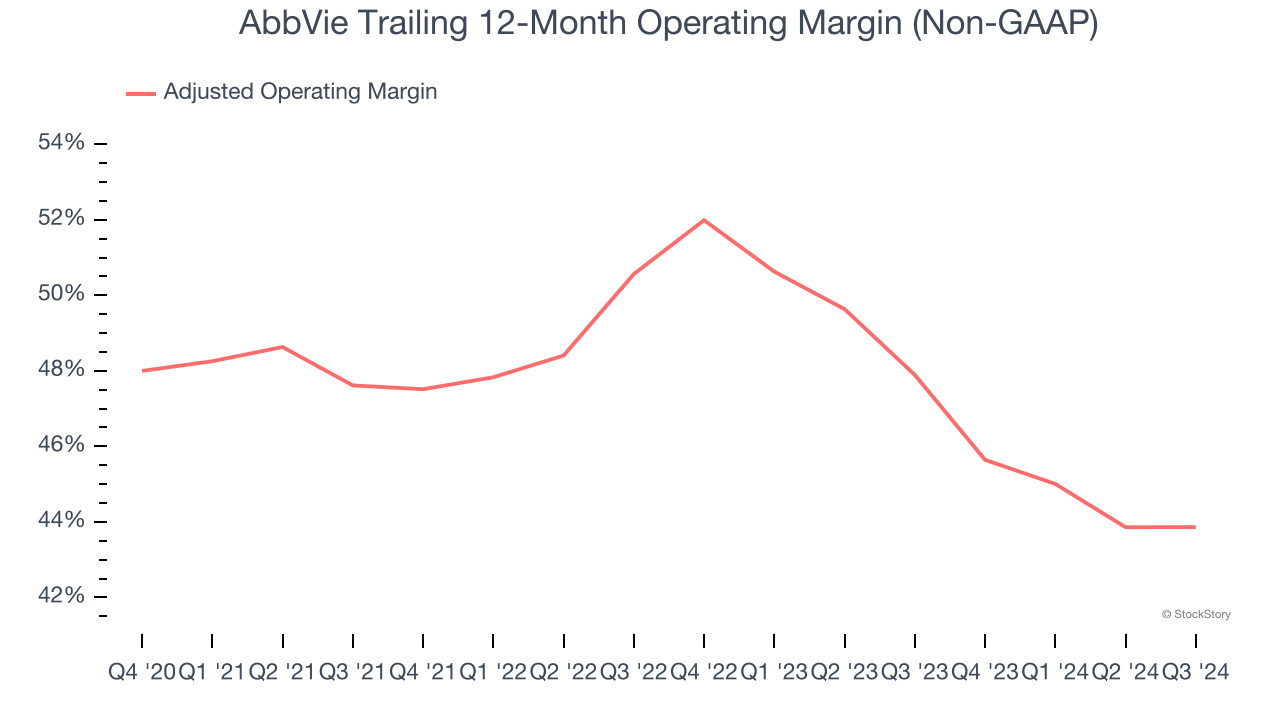

Adjusted Operating Margin

AbbVie has been a well-oiled machine over the last five years. It demonstrated elite profitability for a healthcare business, boasting an average adjusted operating margin of 47.6%.

Analyzing the trend in its profitability, AbbVie’s adjusted operating margin decreased by 4.6 percentage points over the last five years. This performance was caused by more recent speed bumps as the company’s margin fell by 8.1 percentage points on a two-year basis. We’re disappointed in these results because it shows operating expenses were rising and it couldn’t pass those costs onto its customers.

in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

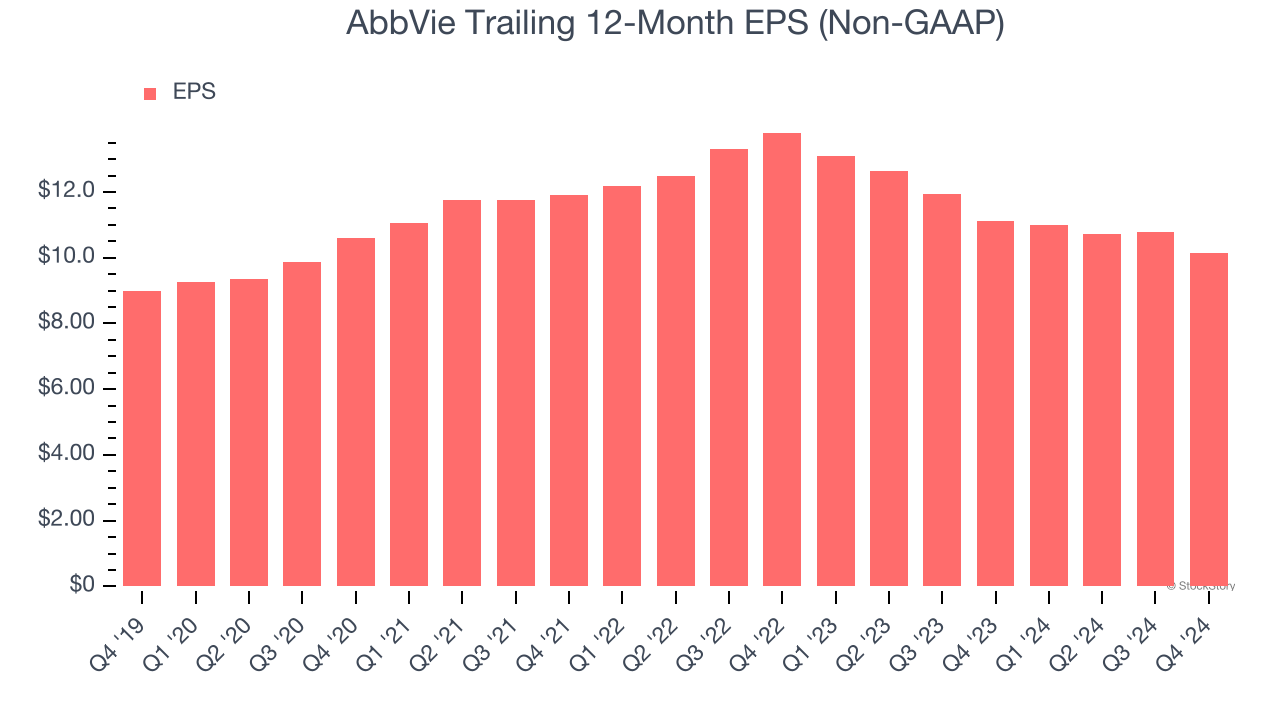

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

AbbVie’s EPS grew at an unimpressive 2.4% compounded annual growth rate over the last five years, lower than its 8.6% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

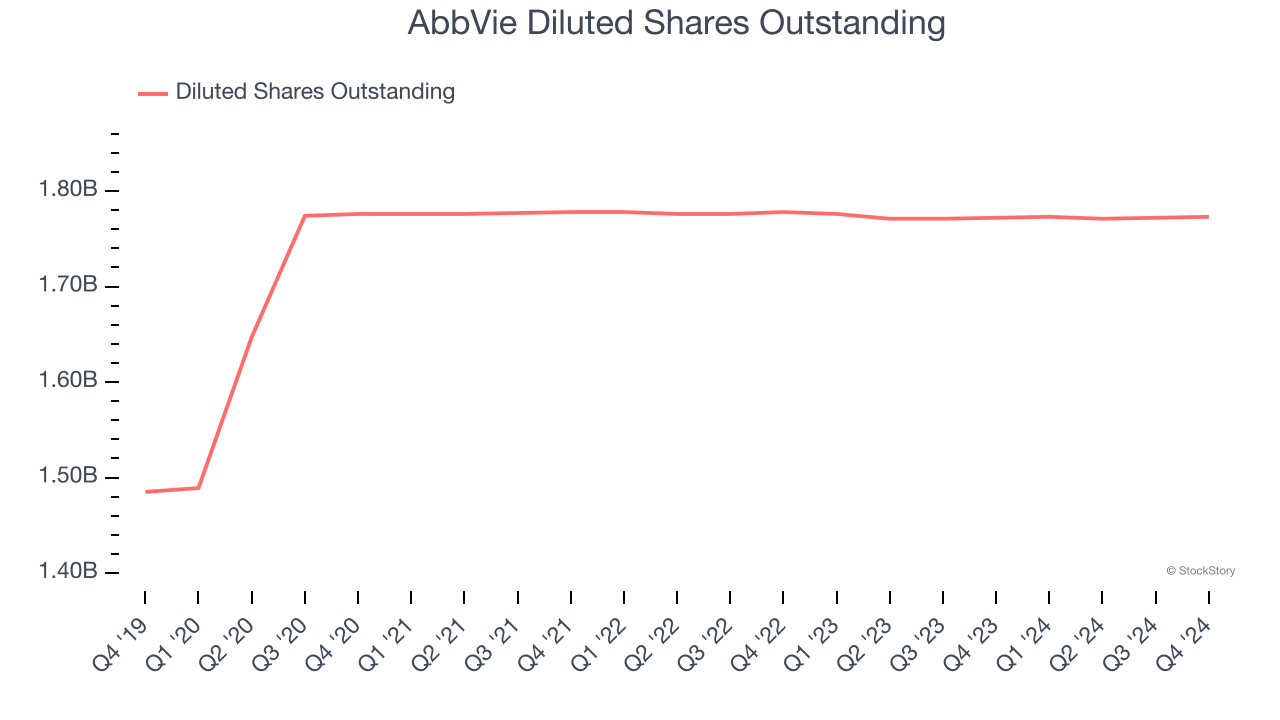

We can take a deeper look into AbbVie’s earnings to better understand the drivers of its performance. As we mentioned earlier, AbbVie’s adjusted operating margin declined by 4.6 percentage points over the last five years. Its share count also grew by 19.4%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q4, AbbVie reported EPS at $2.16, down from $2.80 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects AbbVie’s full-year EPS of $10.13 to grow 21.1%.

Key Takeaways from AbbVie’s Q4 Results

We were impressed by how significantly AbbVie blew past analysts’ constant currency revenue expectations this quarter. We were also happy its 2025 EPS guidance outperformed Wall Street’s estimates. Overall, this quarter had some key positives. The stock traded up 5.3% to $184.84 immediately after reporting.

So do we think AbbVie is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.