Advanced Micro Devices (NASDAQ: AMD) isn’t getting the attention some stocks in the semiconductor industry are, but it should not be counted out. Multiple factors suggest a solid upside in 2024; it could top 50% by year-end. Among the factors are the rise of AI, demand for data center infrastructure, AI at the edge and normalization in end markets that has the entire industry on track for growth. The latest data from the SIA suggests semiconductor revenue growth will top 13% for the year, led by AI.

The takeaway for investors is that AMD’s outlook for 2024 is sufficient to keep the stock advancing but underestimates the potential for gains. Analysts forecast a mere 17% revenue growth, solid enough on its own, but this is pale compared to the gains posted by NVIDIA (NASDAQ: NVDA).

NVIDIA is the leader in data centers and AI accelerators but cannot meet demand, sending its revenue up triple digits. NVIDIA’s inability to meet the demand for chips was seen clearly in Oracle’s (NYSE: ORCL) FQ2/CQ3 results, which fell short of consensus due to insufficient capacity and a shortfall of chips, not because of demand for its cloud-based services. That is an opportunity for AMD to gain market share that it will not let slip by.

Advanced Micro Devices aims to take share from NVIDIA

Advanced Micro Devices MI300 line is coming into availability soon. Lenovo (OTCMKTS: LNVGY) recently announced support for the series, with planned availability in the first half of the year. Demand for the chips is expected to be solid, with names like Oracle, Lenovo, Dell (NYSE: DELL), Microsoft (NASDAQ: MSFT), Meta Platforms (NASDAQ: META) and others on board. Advanced Micro Devices should easily exceed CEO Lisa Su’s forecast for $2 billion in sales in the first year as it nabs market share from NVIDIA.

The risk is manufacturing. NVIDIA and Advanced Micro Devices rely heavily on Taiwan Semiconductor Manufacturing (NYSE: TSM) for their advanced AI chip manufacturing. Taiwan Semiconductor has already stated that it will be well into 2025 before it can catch up with AI demand, posing a hurdle for NVIDIA and AMD.

However, AMD relies less on Taiwan-based manufacturers for its advanced packaging; instead, it turns to China-based Tongfu Microelectronics, which may make all the difference. Taiwan Semiconductor is reportedly outsourcing some of its processes, which may lengthen lead times for NVIDIA.

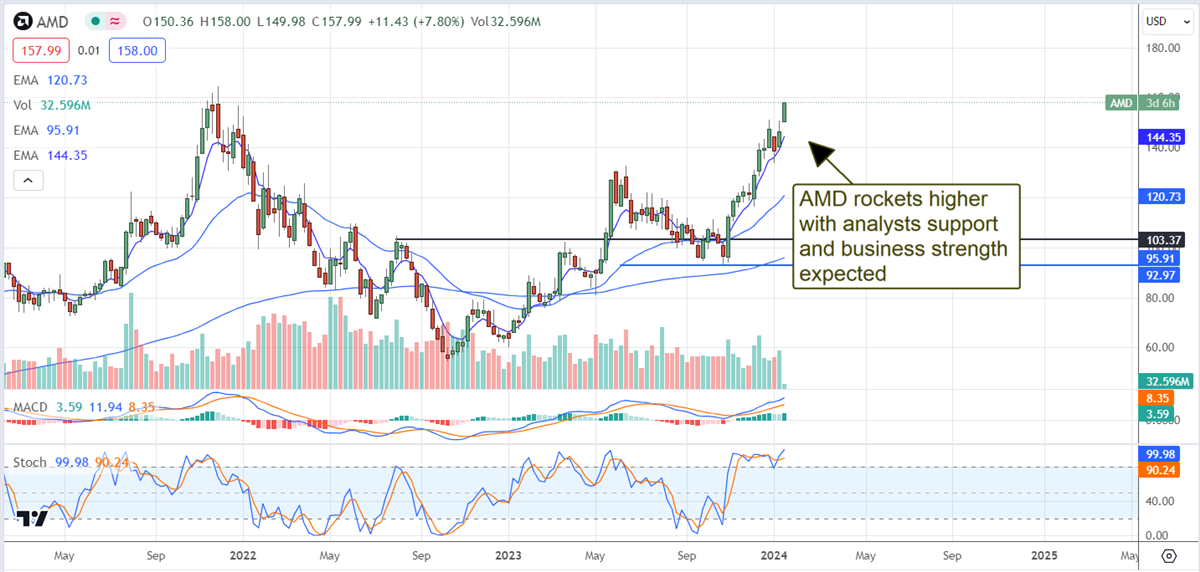

Analysts lead Advanced Micro Devices share price upward

Analyst's activity in AMD stock is bullish and leading the market higher. The company received some mixed reviews in 2023 but the trend in sentiment has the consensus edging up from Moderate Buy to Buy and the price target up 45% YOY. The consensus target is up 5% in January and is likely to move higher, based on the chatter.

Takeaways from reports issued by Barclays (NYSE: BCS), Goldman Sachs (NYSE: GS), Bank of America (NYSE: BAC), and Wells Fargo (NYSE: WFC) suggest the 2nd wave of AI is upon us; AMD is a strategic opportunity with significant upside potential in Q1 and a top-10 efficient growth stock supported by secular tailwinds. The only negative detail is that the consensus price target lags the market, but the trend in sentiment offsets it.

The latest price revisions include the highest target of $141, which is 45% above current market action and leading the market. Because AMD’s Q4 forecasts are tepid, the company will likely outperform consensus forecasts for revenue and earnings and sustain the trend in upward price target revisions.

The technical outlook points to a 50% upside

All else aside, the price action in AMD is robust and points to at least a 50% upside. The price action in 2023 was tepid; the stock corrected but put in a solid bottom and bounced higher in the 2nd half. That bounce produced a strong rally that increased the price by 51% or about $50. Projecting those gains onto the consolidation and continuation pattern that is forming now gives a target of $200 to $217, aligning with the high end of the analysts' range and a 33% to 50% upside.