Sends Letter Highlighting Benefits of Amended Transactions and Enhanced Opportunities for Shareholder Participation

Refutes Misleading Claims from Ortelius and Invictus and Makes Clear There are No Credible, Actionable Financing Alternatives on the Table

Notes that the Terms of the Invictus Proposal are Highly Conditional and Would Add Leverage to Company at a Time When the Exact Opposite is Needed

Urges Shareholders to Support Amended Transactions by Voting on the WHITE Card at Special Meeting on October 22, 2021

Capital Senior Living Corporation (“Capital Senior Living” or the “Company”) (NYSE: CSU), a leading owner-operator of senior living communities across the United States, today sent a letter to its shareholders setting the record straight around its plans to raise up to $154.8 million through a series of recently amended financing transactions between the Company and Conversant Capital (the “Amended Transactions”).

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20211007006066/en/

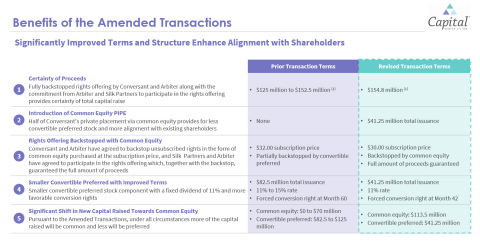

(Graphic: Business Wire) Figure 1 (1) Represents initial capital raise exclusive of incremental $25 million accordion

The Company also recently issued a supplemental presentation rebutting several misleading and factually inaccurate claims made in recent public statements by Ortelius Advisors (“Ortelius”) and Invictus Global Management (“Invictus”), which is available at https://www.sec.gov/Archives/edgar/data/1043000/000119312521293772/d243110ddefa14a.htm.

The full text of the letter is below.

October 7, 2021

Dear Capital Senior Living Shareholders,

As you know, we will hold a Special Meeting of Stockholders (the “Special Meeting”) on October 22, 2021, to approve plans to raise up to $154.8 million through the combination of:

- The private placement of convertible preferred stock, common stock and warrants to Conversant Capital (“Conversant”);

- An amended common stock rights offering to our existing stockholders, with a revised subscription price of $30 per share; and

- An incremental $25 million accordion from Conversant for future investment at the Company’s option, subject to certain conditions (collectively, the “Amended Transactions”).

We, the members of your Board of Directors (the “Board”), believe that the Amended Transactions are in the best interests of shareholders and are writing today to strongly urge you to support the Amended Transactions to protect your investment in the Company.

The Reality is Simple

- CSU is over-levered, with no unencumbered assets. Based on our current cash burn and near-term liabilities, the Company will likely run out of cash by year-end.

- The Amended Transactions provide immediate liquidity to address working capital deficits, fund greatly needed capital expenditures, resolve near-term debt maturities, and stabilize the Company.

- There are no credible, actionable and immediate alternatives to the Amended Transactions that will resolve the Company’s urgent need for significant capital.

- Voting against the Amended Transactions likely will send the Company down the path of insolvency.

Unfortunately, recent public statements by Ortelius Advisors (“Ortelius”) and Invictus Global Management (“Invictus”) contain numerous misleading claims regarding the Company’s financial situation and the Amended Transactions. It is not in the best interests of CSU or its shareholders to respond point-by-point to the activist investors’ attacks on the Company, its Board and its advisors – but it is critical that shareholders understand the facts:

Ortelius’ Claims Misrepresent the Availability of Alternative Capital

Two existing, large shareholders Arbiter Partners (“Arbiter”) and Silk Partners (“Silk”) previously didn’t provide any commitment to backstop or participate in the transactions, and have only recently committed to do so (a) with significant right-sizing of the equity component of the capital structure and (b) given their confidence in the strategic value brought by a long-term oriented investor in Conversant. Arbiter and Silk’s commitments are not transferable. They have committed capital to the Amended Transactions, which were fully diligenced by Conversant and negotiated by the Company – not a hypothetical proposal from Ortelius.

In its October 6th presentation, Ortelius blatantly and recklessly misrepresents the facts by suggesting alternative, committed capital exists with no further due diligence required.1 This is simply not true.

With regard to Ortelius, its purported capital commitment includes no disclosure around terms, source or conditionality. And this is after 8 weeks of Ortelius publicly and aggressively opposing the proposed transactions and canvassing the markets for a capital source. Vague public “commitments” are not a standard that shareholders should be willing to accept, particularly when the continued viability of your company is at stake.

With regard to Invictus, in its October 6th public letter to the Company, Invictus explicitly states that its terms are subject to extensive diligence and conditions, including satisfactory appraisals, a maximum 75% LTV test and satisfactory evaluation and approval of a 13-week cash flow budget.2 Importantly, Invictus’ proposal of all debt financing would also be contingent upon affirmative consent of all the Company’s existing lenders due to junior lien requirement (which we are highly unlikely to receive).

Even if the Invictus Proposal was Actionable (And It is Not), It is Not Superior

In addition to being highly conditional, the Invictus proposal would also compound the already significant financial challenges of the Company by incurring even more excess leverage.

Specifically, Invictus is proposing a capital raise solely in the form of debt, at a time when the Company is significantly over levered and cash flow negative. With a debt to total market capitalization ratio of 91%, as well as sizable near-term maturities, it is quite clear that we need to reduce leverage, not increase it as proposed by Invictus. Adding ~$150+ million of new capital in the form of expensive debt with hard maturities is the exact opposite of what the Company needs right now.

Further, the Invictus proposal is not more favorable for common shareholders. All of Invictus’ capital would be senior to existing shareholders, and their proposed structure prioritizes payments to them over sustainable investment and growth of the business. On the other hand, the Amended Transactions provide for more than $113 million in the form of common equity, providing significantly better alignment and permanent capital to right size the capital structure.

Finally, Invictus’ proposed debt financing is NOT less expensive than the Amended Transactions. In fact, it is quite costly, the senior note at ~11% is expensive and 6-year convertible senior secured notes with a hard repayment date cannot be compared with convertible preferred equity that has favorable redemption rights and no maturity.

Ortelius Misrepresents --- Dangerously --- CSU’s Financial Situation

The Company faces an immediate and critical need for financing and has warned stockholders about significant doubt that it could continue as a “going concern” since reporting its Q1 2020 financial results. Without a meaningful infusion of capital, the Company is facing a liquidity crisis, the probability of running out of cash and the very real possibility of seeking insolvency relief.

The Company has $68 million of mortgage debt maturing by May 2022 and another $40 million by the end of 2022. These assets are not cash flow positive, are highly leveraged and will require millions of dollars in debt paydown in order to secure refinancing. We are distressed and over levered, with debt-to-market cap of 91%, no unencumbered assets and limited cash on hand.

Ortelius chooses to ignore the detailed financial disclosures provided by the Company each of the last 6 quarters. Its claims are riddled with inconsistencies and fundamental misunderstandings of the business. Despite asserting that the Company does not need substantial capital and should be pursuing a $70 million rights offering and not diluting existing stockholders, Ortelius immediately threw its support behind a $153 million debt financing that is senior to existing equity. These inconsistencies should make shareholders seriously question Ortelius’ credibility and understanding of our current situation.

There is No Real, Actionable Alternative on the Table

Even after the Board’s solicitation of 33 counterparties and Ortelius’ public solicitation of alternatives for approximately eight weeks, no real alternatives have been presented by any party.

As detailed in our proxy, after due diligence, two of the three parties with whom we were discussing potential transactions declined to proceed. A diligence condition (which Invictus’ proposal includes) is highly significant and not something on which we are willing to bet the Company’s future or your investment.

Although it is true that we are prohibited from soliciting or encouraging any alternative proposal, that does not stop a potential partner from privately or publicly communicating a firm, actionable commitment (particularly where, as here, a stockholder (Ortelius) has been running a campaign to solicit one). No one has. Knowing that the Company was engaged in discussions to renegotiate the original Conversant deal, Ortelius could have proposed changes – or an alternative – and did neither. Ortelius has chosen not to be constructive; as explained in the proxy, they signed an NDA and were provided an opportunity to discuss the Amended Transactions, and they chose not to engage until publicly responding more than a week later.

The Amended Transactions Have Significantly Improved Terms and a Structure that Enhances Alignment with Shareholders

The Amended Transactions clearly benefit shareholders and address many of the concerns previously expressed. They reflect extensive engagement with shareholders and include the participation of two of the Company’s largest holders – Silk Partners (15.2%) and Arbiter Partners (13.5%). Benefits of the Amended Transactions include certainty of proceeds, the introduction of a common equity PIPE, a rights offering fully backstopped with common stock rather than convertible preferred, a smaller convertible preferred component with improved terms, and a significant shift in new capital raised towards common equity. (See Figure 1.)

The reality is simple: Voting FOR the Amended Transactions is voting for a sustainable future for CSU.

We strongly urge you to vote FOR the Amended Transactions at the upcoming Special Meeting.

Sincerely,

The Capital Senior Living Board of Directors

No Offer or Solicitation / Additional Information and Where to Find It

This press release does not constitute an offer to sell or the solicitation of an offer to buy any securities, nor will there be any sale of any securities in any state or other jurisdiction in which such offer, solicitation, or sale would be unlawful prior to registration or qualification under the securities laws of any such state or jurisdiction. The amended rights offering will be made pursuant to the Company’s shelf registration statement on Form S-3, which became effective on May 6, 2020, a prospectus supplement containing the detailed terms of the rights offering filed with the SEC on September 10, 2021, and an amendment to the prospectus supplement to be filed with the SEC. Any offer will be made only by means of a prospectus and prospectus supplement forming part of the registration statement. Investors should read the prospectus and prospectus supplement and consider the investment objective, risks, fees and expenses of the Company carefully before investing. Copies of the prospectus and prospectus supplement may be obtained at the website maintained by the SEC at www.sec.gov.

In connection with the proposed transaction with Conversant, the Company filed a proxy statement with the SEC on August 31, 2021 and filed an amendment to the proxy statement with the SEC on October 4, 2021. The Company may also file other relevant documents with the SEC regarding the proposed transaction. The proxy statement, and any amendments thereto, have been and will be delivered to stockholders of the Company. This communication is not a substitute for the proxy statement or any other document that may be filed with the SEC in connection with the proposed transaction.

INVESTORS AND STOCKHOLDERS OF THE COMPANY ARE URGED TO READ THE PROXY STATEMENT, AS AMENDED, AND ANY OTHER RELEVANT DOCUMENTS THAT MAY BE FILED WITH THE SEC, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THESE DOCUMENTS, CAREFULLY AND IN THEIR ENTIRETY IF AND WHEN THEY BECOME AVAILABLE BECAUSE THEY CONTAIN OR WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED TRANSACTION.

Investors and security holders are able to obtain free copies of the definitive proxy statement, and when available, the amendment to the proxy statement and other documents containing important information about the Company and the proposed transaction through the website maintained by the SEC at www.sec.gov.

Participants in the Solicitation

The Company and its executive officers and directors and certain other members of management and employees may, under the rules of the SEC, be deemed to be “participants” in the solicitation of proxies in connection with the proposed transaction. Information regarding the Company’s directors and executive officers is available in its Proxy Statement on Schedule 14A for its 2020 Annual Meeting of Stockholders, filed with the SEC on November 3, 2020, and in its Annual Report on Form 10-K for the year ended December 31, 2020, filed with the SEC on March 31, 2021, as amended on April 30, 2021. These documents may be obtained free of charge from the sources indicated above. Other information regarding the participants in the proxy solicitation and a description of their direct and indirect interests, by security holdings or otherwise, is contained in the proxy statement and other relevant materials relating to the proposed transaction filed with the SEC.

About Capital Senior Living

Dallas-based Capital Senior Living Corporation is one of the nation’s leading operators of independent living, assisted living and memory care communities for senior adults. The Company operates 75 communities that are home to nearly 7,000 residents across 18 states providing compassionate, resident-centric services and care and engaging programming. The Company offers seniors the freedom and opportunity to successfully, comfortably and happily age in place. For more information, visit http://www.capitalsenior.com or connect with the Company on Facebook or Twitter.

About Conversant

Conversant Capital LLC is a private investment adviser founded in 2020. The firm pursues credit and equity investments in the real estate, digital infrastructure and hospitality sectors in both the public and private markets. Further information is available at www.conversantcap.com.

Safe Harbor

The forward-looking statements in this press release are subject to certain risks and uncertainties that could cause the Company’s actual results and financial condition to differ materially, including, but not limited to, the Company’s ability to obtain stockholder approval for the proposed transaction; the satisfaction of all conditions to the closing of the proposed transaction; other risks related to the consummation of the proposed transaction, including the risk that the transaction will not be consummated within the expected time period or at all; the costs related to the proposed transaction; the impact of the proposed transaction on the Company’s business; any legal proceedings that may be brought related to the proposed transaction; the continued spread of COVID-19, including the speed, depth, geographic reach and duration of such spread; new information that may emerge concerning the severity of COVID-19; the actions taken to prevent or contain the spread of COVID-19 or treat its impact; the legal, regulatory and administrative developments that occur at the federal, state and local levels in response to the COVID-19 pandemic; the frequency and magnitude of legal actions and liability claims that may arise due to COVID-19 or the Company’s response efforts; the impact of COVID-19 and the Company’s near-term debt maturities on the Company’s ability to continue as a going concern; the Company’s ability to generate sufficient cash flows from operations, additional proceeds from debt refinancings, and proceeds from the sale of assets to satisfy its short and long-term debt obligations and to fund the Company’s capital improvement projects to expand, redevelop, and/or reposition its senior living communities; the Company’s ability to obtain additional capital on terms acceptable to it; the Company’s ability to extend or refinance its existing debt as such debt matures; the Company’s compliance with its debt agreements, including certain financial covenants, and the risk of cross-default in the event such non-compliance occurs; the Company’s ability to complete acquisitions and dispositions upon favorable terms or at all, including the transfer of certain communities managed by the Company on behalf of other owners; the Company’s ability to improve and maintain adequate controls over financial reporting and remediate the identified material weakness; the risk of oversupply and increased competition in the markets which the Company operates; the risk of increased competition for skilled workers due to wage pressure and changes in regulatory requirements; the departure of the Company’s key officers and personnel; the cost and difficulty of complying with applicable licensure, legislative oversight, or regulatory changes; the risks associated with a decline in economic conditions generally; the adequacy and continued availability of the Company’s insurance policies and the Company’s ability to recover any losses it sustains under such policies; changes in accounting principles and interpretations; and the other risks and factors identified from time to time in the Company’s reports filed with the Securities and Exchange Commission.

View source version on businesswire.com: https://www.businesswire.com/news/home/20211007006066/en/

Contacts

Media Inquiries:

Dan Zacchei / Joe Germani

Sloane & Company

dzacchei@sloanepr.com / jgermani@sloanepr.com

Investor Inquiries:

Chris Hayden

Georgeson LLC

(212) 440-9850, chayden@georgeson.com

Company:

Capital Senior Living

Kimberly Lody

President and Chief Executive Officer

(972) 308-8323, klody@capitalsenior.com