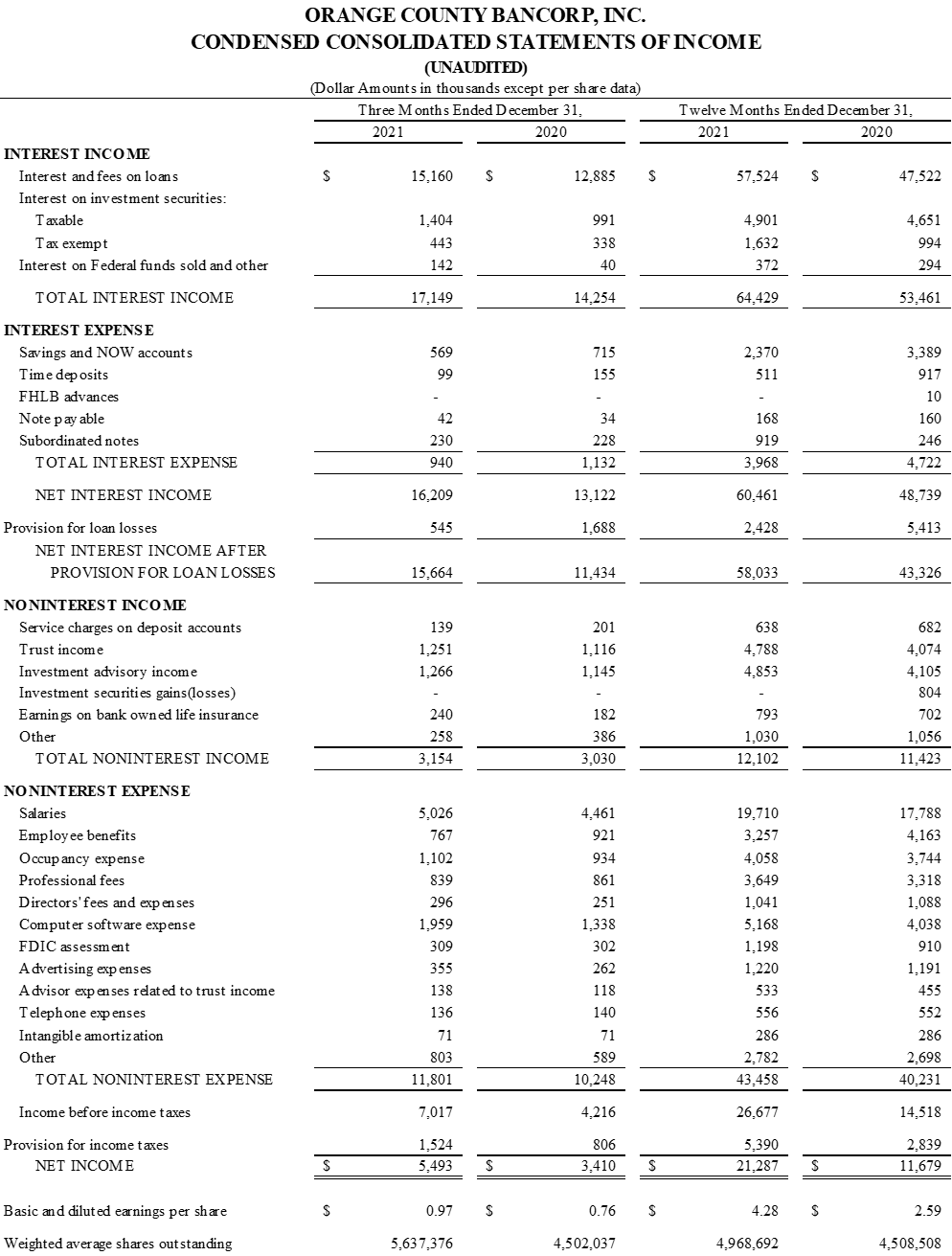

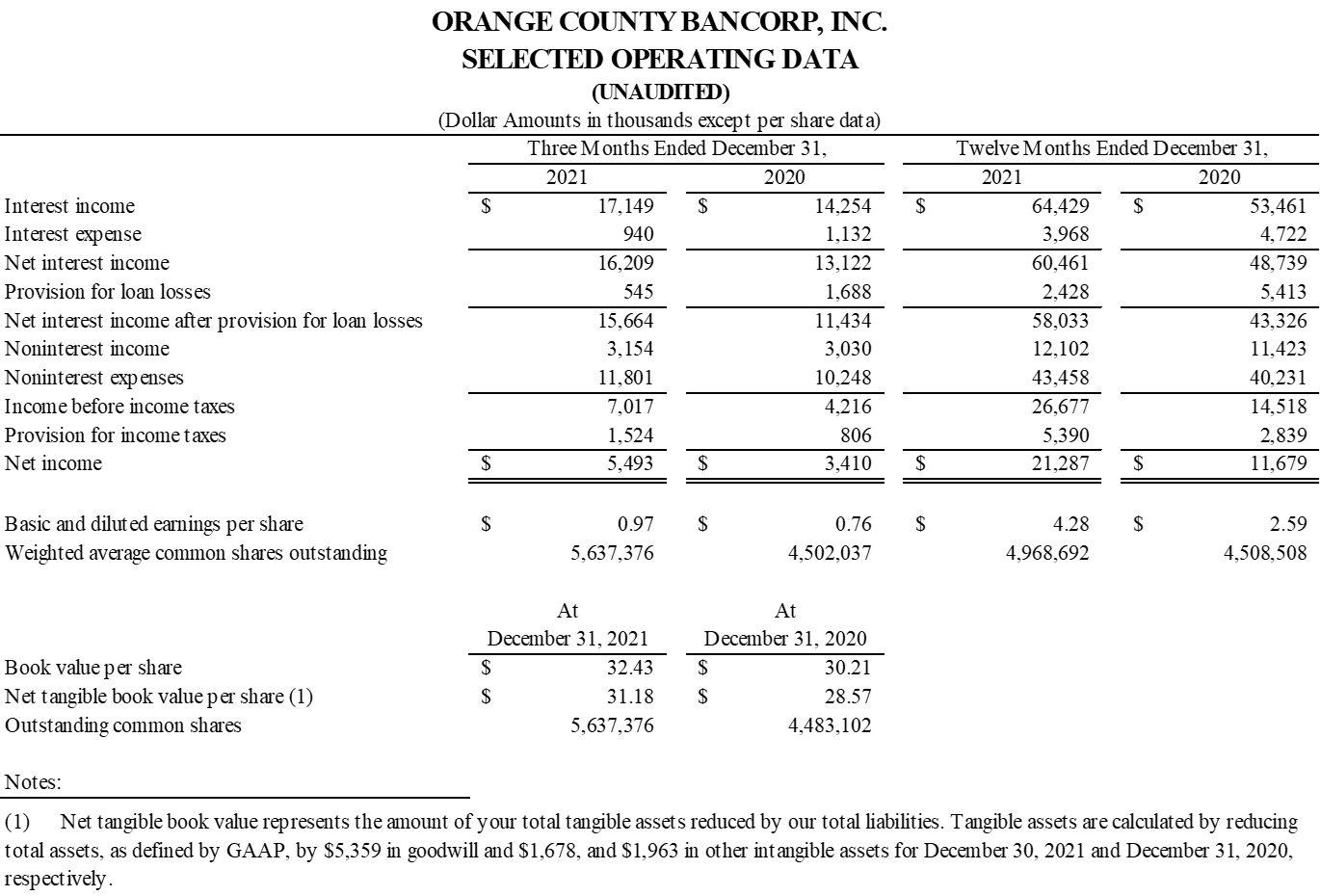

- Net Income for full year 2021 increased $9.6 million, or 82.1%, to a record $21.3 million

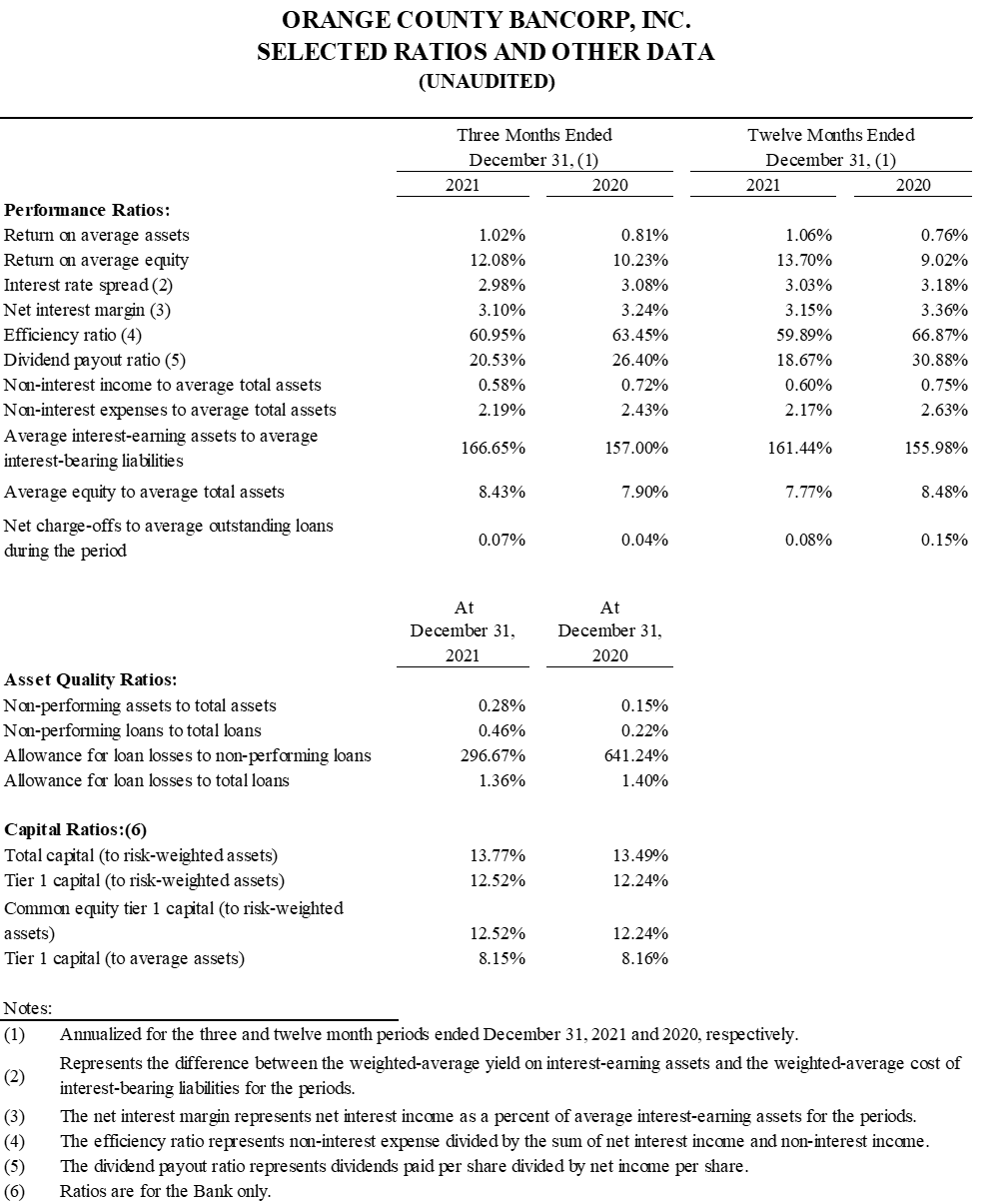

- Return on average assets for Q4 2021 rose 21 basis points, or 25.9%, year-over-year to 1.02%

- Return on average equity for Q4 2021 rose 185 basis points, or 18.1%, year-over-year to 12.08%

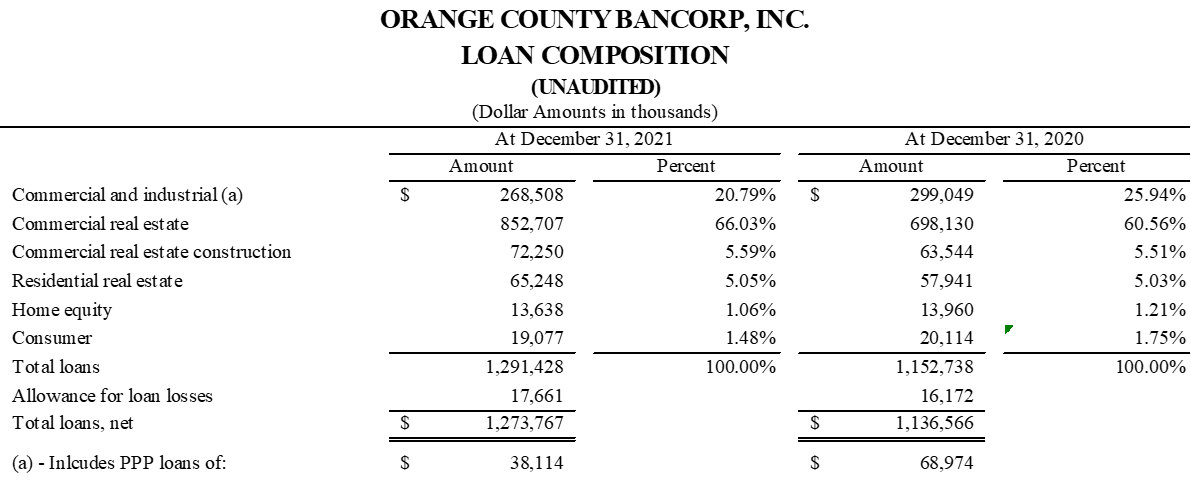

- Average Loans (net of PPP) for Q4 2021 increased approximately 20% year-over-year, to $1.2 billion

- Provision for loan losses of $545 thousand for Q4 2021 declined 67.7% year-over-year due to stabilizing credit trends and characteristics within the portfolio

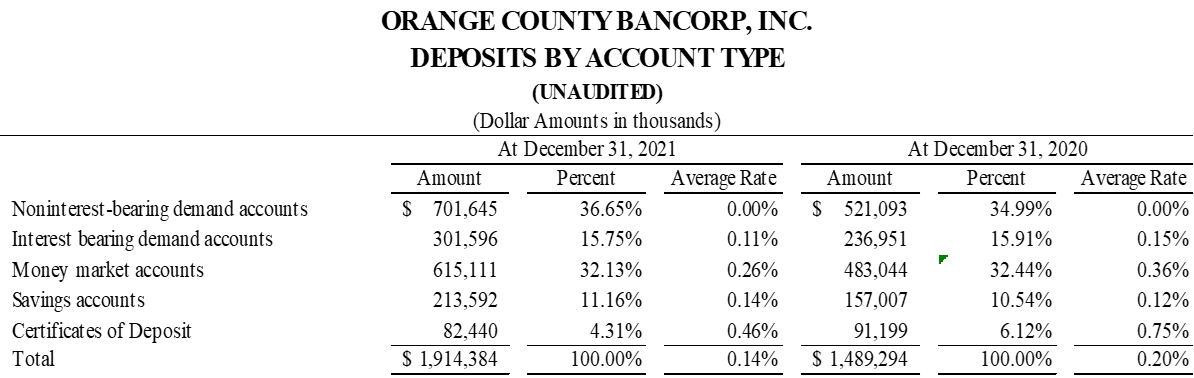

- Average demand and money market deposits for Q4 2021 grew 25.8% year-over-year to $949.3 million

- Total Assets grew $476.1 million, or 28.6%, from year-end 2020 to $2.1 billion at December 31, 2021

- Trust and asset advisory business revenue increased 17.9% year-over-year, to $9.6 million, for year end 2021

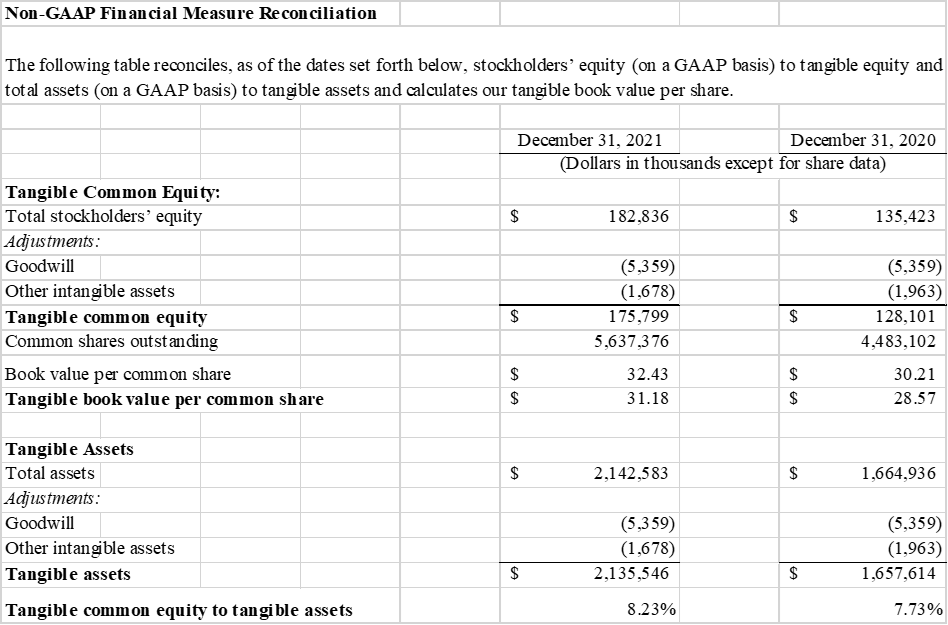

- Book Value per Share rose $2.22, or 7.4%, to $32.43 at December 31, 2021 compared to $30.21 at December 31, 2020

- Net Tangible Book Value per Share rose $2.61, or 8.6%, to $31.18 at December 31, 2021 compared to $28.57 at December 31, 2020

MIDDLETOWN, NY / ACCESSWIRE / January 26, 2022 / Orange County Bancorp, Inc. (the "Company")(NASDAQ:OBT), parent company of Orange Bank & Trust Co. (the "Bank") and Hudson Valley Investment Advisors, Inc. ("HVIA"), today announced net income of $5.5 million, or $0.97 per basic and diluted share, for the three months ended December 31, 2021. This compares with net income of $3.4 million, or $0.76 per basic and diluted share, for the three months ended December 31, 2020. For the year ended December 31, 2021, net income increased by $9.6 million, or 82.1%, over the prior year, to $21.3 million, or $4.28 per basic and diluted share. This compares with net income of $11.7 million, or $2.59 per basic and diluted share, for the year ended December 31, 2020.

"Over the past several years Orange County Bancorp has strategically positioned itself as the premier business bank in the region," said Orange County Bancorp President & CEO, Michael Gilfeather. "We recognized early on that the decentralized banking model employed by many of our competitors left small and midsized businesses in the communities we serve without a true banking partner. We have sought to fill that void and I am pleased to announce our record results for the quarter and year just ended demonstrate the success of our strategy. Net income of $21.3 million in 2021 represents an increase of $9.6 million, or approximately 82%, for the year.

Key to delivering on our superior value proposition to business clients were contributions from all parts of the bank. I am also pleased to report that every business segment shared in our growth, with the Bank's loan portfolio increasing more than 12%, to $1.3 billion, and our deposit base increasing more than 28%, to $1.9 billion.

Our loan growth was, in fact, even stronger than the headline number suggests, as a substantial portion of PPP (Paycheck Protection Program) loans originated over the past 18 months were forgiven this year. At year end, these loans totaled just $38.1 million, down from a high of $123.9 million in April 2021. As I've mentioned previously, this was a program we were very proud of to have championed on behalf of our clients and, as it turned out, served as a critical life line for many. After almost two years of loan deferrals related to the impact of the COVID pandemic, we finished 2021 with no loan deferrals within our portfolio.

To ensure our strict underwriting and risk management standards kept pace with our growth, we upgraded our data and accounting systems during the year. We completed this project in the 4th quarter and it came in at approximately $725 thousand, well below our nearly $900 thousand cost estimate.

Early last year we also launched our Wealth Management initiative, integrating the expertise of our Private Banking, Trust and Investment Advisory Service businesses to create a comprehensive offering for clients with complex business or financial and estate planning needs. In keeping with our strategic business focus, we have tailored Wealth Management to serve our new and existing business relationships. The results to date have been very encouraging, with revenues growing approximately 18% for the year to $9.6 million.

As we have gained experience and confidence partnering with local business communities through our expansion efforts, we have developed a better understanding of where and how to effectively grow the Bank. In July, we opened a branch in the Bronx, which in its short history has performed well above expectations. We also opened a branch in Nanuet in November, positioning us to better serve Rockland County and, given its proximity to New Jersey, gaining visibility into Bergen County. We are very excited about the prospects for these branches and continue to evaluate other areas for potential expansion.

To bolster implementation of our growth strategy, we launched and announced a successful completion of an initial public offering of common stock in early Q3 2021. The transaction was upsized due to strong institutional demand and culminated in the sale of 1.15 million shares at a price of $33.50 per share, for gross proceeds of approximately $38.5 million. Our shares now trade on the NASDAQ Capital Market under the symbol "OBT". In addition to providing growth capital, the transaction also raises the Company's visibility with investors, enhancing liquidity and shareholder diversification and, if necessary, offering more efficient access to capital in the future. We believe these factors and others have helped unlock value in our stock since the offering.

The success we enjoyed in 2021 was the result of years of planning and investment in facilities, technology, and personnel. None of it, however, would have been possible without the commitment and effort of every employee of the Bank. The foundation for responsibly growing our business remains strong, and I am confident our team will continue to deliver exceptional service to our clients and the communities we serve. This, in turn, should create additional opportunities to grow the Bank and generate even stronger results for our shareholders. I am incredibly fortunate to be surrounded by such a team and thank them for their hard work."

Fourth Quarter and Full-Year 2021 Financial Review

Net Income

Net income for the fourth quarter of 2021 was $5.5 million, an increase of approximately $2.1 million, or 61.8%, over net income of $3.4 million for the fourth quarter of 2020. Net income for the twelve months ended December 31, 2021 was $21.3 million, an increase of $9.6 million, or 82.1%, over net income of $11.7 million for the prior year. Growth for the fourth quarter and full year 2021 continued to be driven primarily by increases in net interest income and non-interest income and a decrease in the provision for loan losses, partially offset by increases in non-interest expense and provision for income taxes.

Net Interest Income

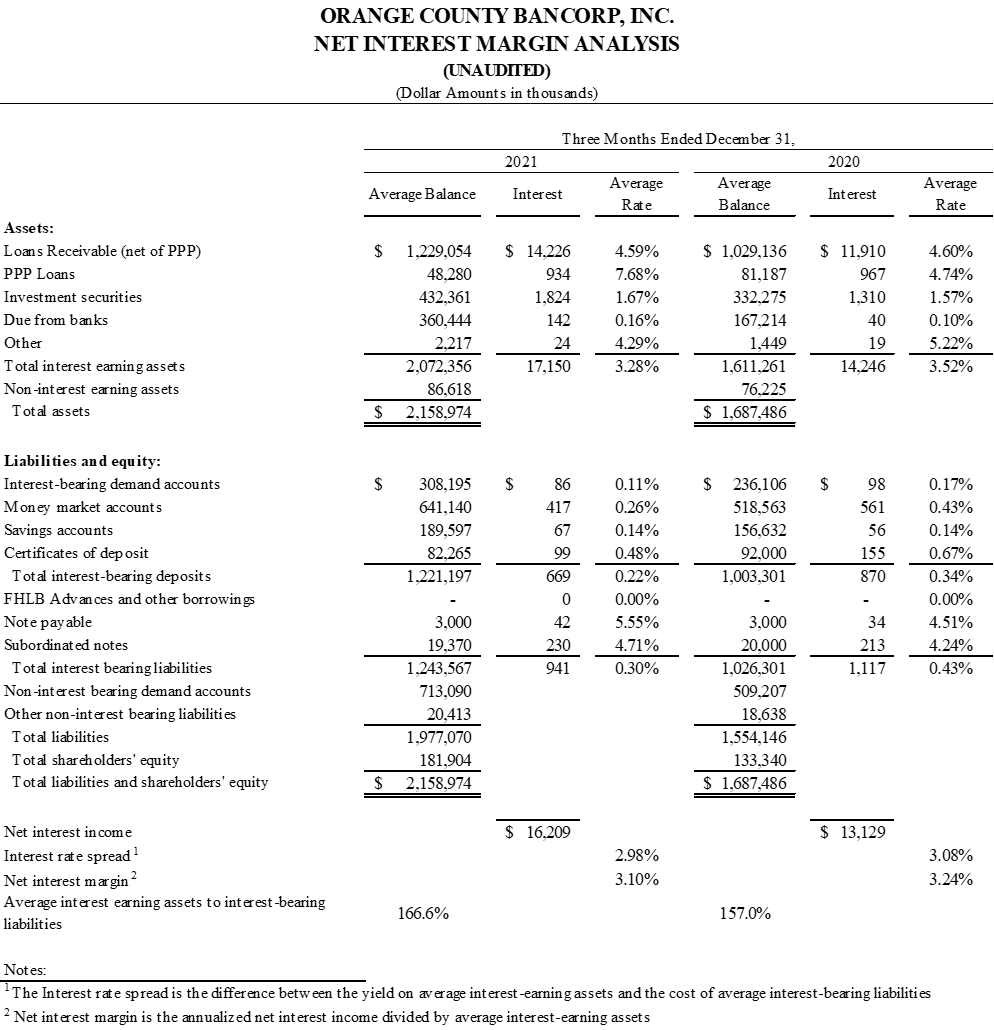

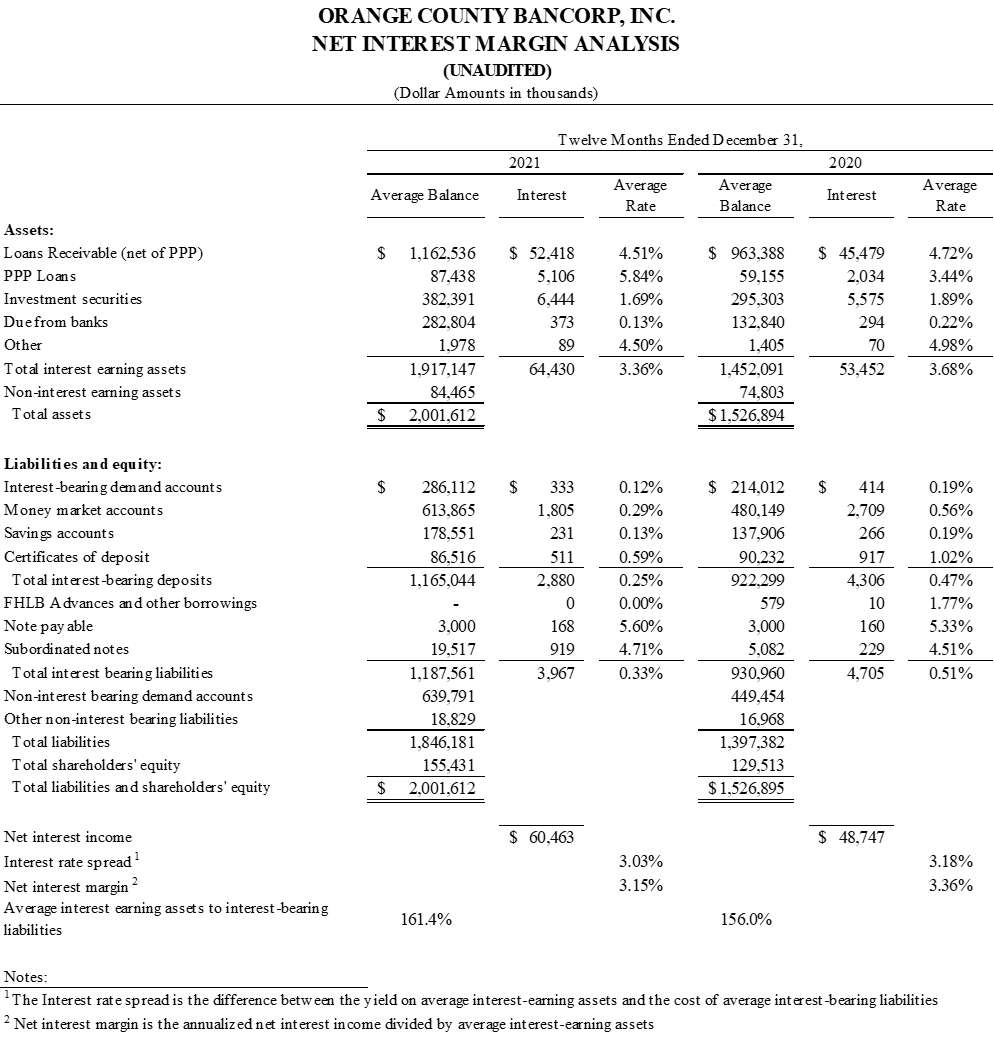

For the three months ended December 31, 2021, net interest income increased by $3.1 million, or 23.7%, to $16.2 million versus the same period last year. For the twelve months ended December 31, 2021, net interest income increased by $11.7 million, or 24.0%, to $60.5 million as compared to the same period last year.

Total interest income increased $2.9 million, or 25.7%, to $17.1 million and $10.9 million, or 20.4%, to $64.4 million for the three and twelve months ended December 31, 2021, respectively, versus the corresponding periods last year. The increase in interest income was primarily due to loan growth and fees associated with PPP loan forgiveness.

Total interest expense decreased $192 thousand in the fourth quarter of 2021, to $940 thousand, as compared to $1.1 million in the fourth quarter of 2020, and decreased $754 thousand for the twelve months ended December 31, 2021, to $4.0 million from $4.7 million for the twelve months ended December 31, 2020. The decrease resulted from a reduction in deposit interest expense partially offset by an increase in interest expense due to subordinated debt issued in Q3 2020. Lower interest expense on deposits, even with 26% average year-over-year growth, was consistent with reduction of the Fed Funds rate in the first quarter of 2020 in response to the COVID-19 pandemic and continued low rates within the Bank's market.

Provision for Loan Losses

The Company recognized provisions for loan losses of $545 thousand and $2.4 million for the three and twelve months ended December 31, 2021, respectively, compared to $1.7 million and $5.4 million for the three and twelve months ended December 31, 2020. The lower provisions reflected continued improvements in credit metrics as well as a reduction in loan deferrals during Q4 2021. The allowance for loan losses to total loans was 1.36% as of December 31, 2021 and 1.40% as of December 31, 2020. Excluding PPP loans, the ratios were 1.41% and 1.49% as of the same dates, respectively.

Non-Interest Income

Non-interest income was $3.2 million for Q4 2021, and represented a $124 thousand increase from $3.0 million for the same period in 2020. Non-interest income rose approximately $679 thousand, to $12.1 million, for the twelve months ended December 31, 2021 as compared to approximately $11.4 million for the same period in 2020. The growth continues to be supported by the increased success of the Bank's trust operations and HVIA asset management activities.

Non-Interest Expense

Non-interest expense was $11.8 million and $10.2 million for the fourth quarters of 2021 and 2020, respectively, reflecting an increase of approximately $1.6 million, or 14.6%, while non-interest expense of $43.5 million for the twelve months ended December 31, 2021, rose $3.3 million, or 8.2%, versus $40.2 million for the same period in 2020. The increase in non-interest expense for the three and twelve month periods was due to our continued investment in growth. This investment consisted primarily of increases in salaries, information technology, professional fees, and deposit insurance costs, the latter due to significant growth in deposit balances. Our efficiency ratio improved to 60.95% for the three months ended December 31, 2021, from 63.45% for the same period in 2020, and to 59.89% for the twelve months ended December 31, 2021, from 66.87% for the twelve months ended December 31, 2020.

Income Tax Expense

Our provision for income taxes for the three months ended December 31, 2021 was $1.5 million, compared to $806 thousand for the same period in 2020. The provision for income taxes for the twelve months ended December 31, 2021 was $5.4 million, compared to $2.8 million for the same period in 2020. The increase for both periods was due to the increase in income before income taxes. Our effective tax rate for the three and twelve month periods ended December 31, 2021 was 21.7% and 20.2%, respectively, versus 19.1% and 19.6%, respectively, for the same periods in 2020.

Financial Condition

Total consolidated assets increased $476.1 million, or 28.6%, from $1.7 billion at December 31, 2020 to $2.1 billion at December 31, 2021. The increase was driven by growth in loans, cash, and investment securities during the year ended 2021.

Total cash and due from banks increased from $121.2 million at December 31, 2020 to $306.2 million at December 31, 2021, an increase of approximately $185.0 million, or 152.6%. This increase resulted primarily from increases in deposit balances driven by seasonal increases in municipal deposits, continued success attracting business account assets, and government efforts to increase liquidity in the economy.

Total investment securities rose $134.7 million, or 40.9%, from $330.1 million at December 31, 2020 to $464.8 million at December 31, 2021. The increase was due to a $117.1 million increase in agency mortgage backed securities, an $15.6 million increase in municipal securities, and a $9.5 million increase in corporate subordinated debt securities, partially offset by an unrealized loss of approximately $7 million in U.S. government securities since December 31, 2020.

Total loans increased $138.7 million, or 12.0%, from $1.15 billion at December 31, 2020 to $1.29 billion at December 31, 2021. The increase was primarily due to $154.6 million of commercial real estate loan growth in 2021. PPP loans declined by $30.9 million to $38.1 million at December 31, 2021 from $69.0 million at December 31, 2020. The majority of the remaining balance of PPP loans is subject to forgiveness.

Total deposits rose $425.1 million, to $1.9 billion, at December 31, 2021, from $1.5 billion at December 31, 2020. This increase continues to be driven primarily by continued success in business account development and PPP loan proceeds combined with municipal deposit growth as well as the government efforts to increase liquidity in the economy.

Stockholders' equity increased $47.4 million, to $182.8 million, at December 31, 2021 from $135.4 million at December 31, 2020. This increase was primarily due to a $34.7 million increase in surplus reflecting net proceeds from our public offering of common stock in August, 2021. In addition, retained earnings rose $17.3 million during the twelve months of 2021 as a result of net income, partially offset by a $5.3 million decline in AOCI due to changes in the market value of investment securities held for sale.

At December 31, 2021, the Bank maintained capital ratios in excess of regulatory standards for well capitalized institutions. The Bank's Tier 1 capital to average assets ratio was 8.15%, both common equity and Tier 1 capital to risk weighted assets were 12.52%, and total capital to risk weighted assets was 13.77%. These ratios reflect a contribution of $17.5 million of capital at the Bank level representing roughly half of the net proceeds from the Company's public offering of common stock.

Loan Quality

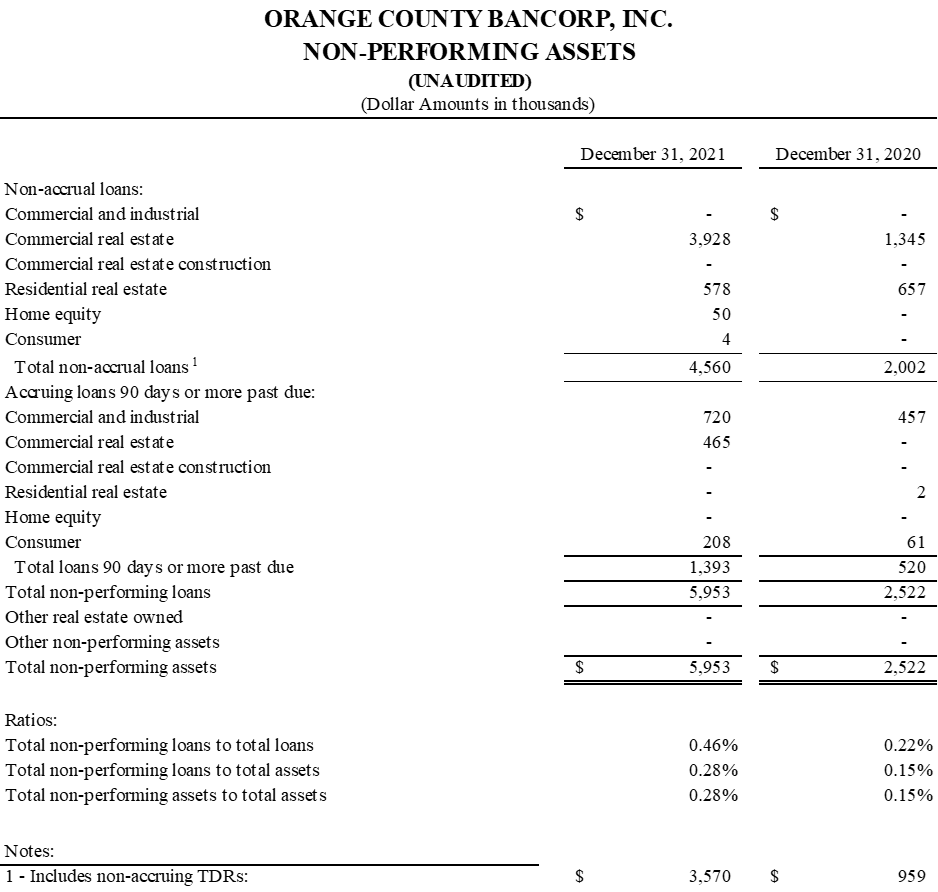

At December 31, 2021, the Bank had total non-accrual loans of $4.6 million, or 0.35% of total loans, which included $3.5 million of Troubled Debt Restructured Loans ("TDRs"). The latter represents 0.28% of total loans, and was $2.6 million greater than year end 2020 as a result of a single, mortgage-secured loan that was placed on non-accrual during the quarter. Accruing loans delinquent greater than 30 days were $4.6 million as of December 31, 2021, as compared to $1.8 million at December 31, 2020.

About Orange County Bancorp, Inc.

Orange County Bancorp, Inc. is the parent company of Orange Bank & Trust Company and Hudson Valley Investment Advisors, Inc. Orange Bank & Trust Company is an independent bank that began with the vision of 14 founders over 125 years ago. It has grown through innovation and an unwavering commitment to its community and business clientele to more than $2.0 billion in total assets. Hudson Valley Investment Advisors, Inc. is a Registered Investment Advisor in Goshen, NY. It was founded in 1996 and acquired by the Company in 2012.

Forward Looking Statements

Certain statements contained herein are "forward looking statements" within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such forward looking statements may be identified by reference to a future period or periods, or by the use of forward looking terminology, such as "may," "will," "believe," "expect," "estimate," "anticipate," "continue," or similar terms or variations on those terms, or the negative of those terms. Forward looking statements are subject to numerous risks and uncertainties, including, but not limited to, those related to the real estate and economic environment, particularly in the market areas in which the Company operates, competitive products and pricing, fiscal and monetary policies of the U.S. Government, changes in government regulations affecting financial institutions, including regulatory fees and capital requirements, changes in prevailing interest rates, credit risk management, asset-liability management, the financial and securities markets and the availability of and costs associated with sources of liquidity. Further, given its ongoing and dynamic nature, it is difficult to predict what the continuing effects of the COVID-19 pandemic will have on our business and results of operations. The pandemic and related local and national economic disruption may, among other effects, continue to result in a material adverse change for the demand for our products and services; increased levels of loan delinquencies, problem assets and foreclosures; branch disruptions, unavailability of personnel and increased cybersecurity risks as employees work remotely.

The Company wishes to caution readers not to place undue reliance on any such forward looking statements, which speak only as of the date made. The Company wishes to advise readers that the factors listed above could affect the Company's financial performance and could cause the Company's actual results for future periods to differ materially from any opinions or statements expressed with respect to future periods in any current statements. The Company does not undertake and specifically declines any obligation to publicly release the results of any revisions that may be made to any forward looking statements to reflect events or circumstances after the date of such statements or to reflect the occurrence of anticipated or unanticipated events.

For further information:

Robert L. Peacock

SEVP Chief Financial Officer

rpeacock@orangebanktrust.com

Phone: (845) 341-5005

SOURCE: Orange County Bancorp, Inc.

View source version on accesswire.com:

https://www.accesswire.com/685703/Orange-County-Bancorp-Inc-Announces-Record-Earnings-for-2021